Five things to consider for Fixed income in 2025

- 28 January 2025 (5 min read)

Fixed income remains an attractive asset class

Yields in fixed income are high versus historical levels – the Bloomberg Global Aggregate index yield level is in the 78th percentile of yields over the past 20 years, and the 88th over the past 10 years1 . Starting yields have a strong correlation to positive total returns over the long-term, thanks to the compounded income attributes of the asset class.

Inflation has reduced dramatically since the post-COVID highs across developed markets and economic growth remains steady, albeit muted. This supports our argument for lower central bank rates, which we expect to materialise over 2025, and should provide an additional boost for fixed income investors over the income component. This will come from both from the capital appreciation and by lessening the impact of the higher interest burden issuers are facing, bolstering their fundamental strength.

While over time the result of interest rates falling will reduce the income received from those bonds, we do not expect it to fall to levels investors saw a decade ago.

At an outright level, yields remain attractive, however credit spreads are tight and there is potential for increased volatility from inflation uncertainty and rising credit risk premiums given the headwinds from geopolitical risks, protectionism, and the delayed impact of the higher yield environment on corporate balance sheets. Taking a flexible approach to allocating and positioning within fixed income will be crucial to navigate the potentially volatile year ahead.

Should investors consider moving away from credit into government bonds?

A typical metric to assess credit market attractiveness is the credit spread over the equivalent government bond. For US investment grade credit, spreads are close to the lowest they have been since before the Global Financial Crisis. US high yield is similarly valued. European IG and HY spreads are less stretched, but still tighter than long term averages. This should flag as a warning signal to credit investors about potential excess returns over government bonds.

However, we argue that the pricing is broadly justified, and do not expect a strong reversal without a meaningful market event.

Falling central banks rates, strong corporate balance sheets and near-term fiscal stimulus across markets should maintain strong fundamentals, providing strong support for investment grade and high yield bonds. Within high yield specifically, we continue to see a trend of more rising stars than fallen angels and for default rates to remain relatively low. For the US market, the average credit quality of high yield issuers has increased in recent years while the overall duration of the market has declined. This helps support structurally lower credit spreads.

In addition, the increased issuance in debt over 2024 and early 2025 has been met with healthy demand from investors looking to allocate to fixed income. Many investors may still be waiting on the sideline, waiting for credit spreads to cheapen before allocating. Any increase in credit spreads could swiftly be met with strong demand from these investors and a re-tightening of spreads.

Having said this, we do not expect spreads to grind much tighter, and therefore excess returns from investment grade and high yield will be limited to the narrow spread pick-up currently available.

On balance, we are more positive on the credit-sensitive investment grade and high yield broad sectors, although will carefully monitor the impact of macroeconomic themes on corporate fundamentals.

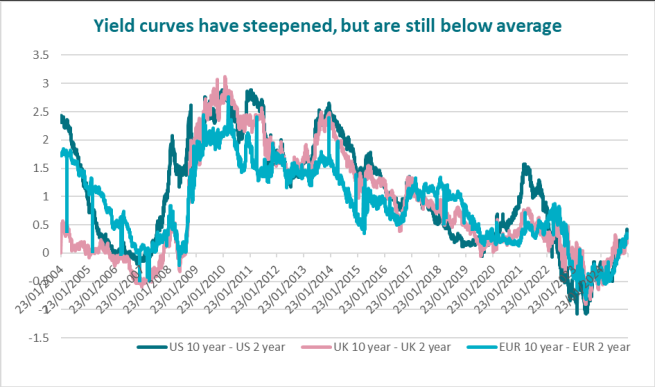

Where are the best opportunities along the curve?

Yield curves have been steadily steepening since the remarkably deep inversion territory seen in 2023 and into 2024. Yields on 10-year governments bonds in the US, the EU and the UK are now broadly 30bps higher than their 2-year equivalent, as shown in the chart below. This is a small additional yield versus historical averages (80-100bps differential).

- U291cmNlOiBBWEEgSU0sIEJsb29tYmVyZyBhcyBvZiAyMiBKYW51YXJ5IDIwMjU=

For investors looking to maximise risk-adjusted returns, short duration bonds appear attractive thanks to:

- The natural liquidity that short duration provides

- The lower interest rate duration naturally bringing lower volatility

- A potential continued steepening of the yield curve - as short end policy rates should continue to ease but long-end yields could remain sticky thanks to expanding fiscal deficits and inflation headwinds

However, the recent positive shift in valuation for longer-maturity bonds has been enough to shift some investors from money markets into short duration, and from short duration into all-maturity strategies. Proponents of all-maturity strategies would argue for the marginal pick up in yield (c.30bps), the lower re-investment risk, and the potential kicker from long term yields falling.

For credit investors, spread curves are slightly steeper than government bond curves, but remain below historical averages, highlighting the continued appetite for the asset class and resulting reduced dispersion across all maturities.

Read more here on why we think short duration is attractive in the current market.

Where to look: Euro vs US credit?

We see both European and US credit as attractive, but for different reasons.

For Europe, we expect the European Central Bank (ECB) will continue monetary easing in 2025, cutting its deposit rate to 1.5% by the end of 2025, possibly sooner. This monetary easing reflects softer growth (est. 1.0% in 2025) in Europe but for bond investors this, alongside solid corporate fundamentals, has the potential upside of stronger total returns as yields decline. This monetary easing needs to be counterbalanced against the softer growth outlook we have for the region (2.3% in 2025) and the impact on any tariffs and trade wars on trade-sensitive sectors. We expect to see a strong dollar continue, so for non-dollar investors, on a currency hedged basis, European fixed income, particularly the opportunities in credit, look attractive.

Meanwhile in the US, the outlook will be determined by Trump’s policies. While it is uncertain what effect they will have, it is more likely to impact growth in 2026. Inflation is the primary concern for 2025, and could restrict the Federal Reserve’s (Fed) ability to ease and may lead to a slower pace of disinflation more broadly. 2025 US growth should remain resilient or even improve. This short-term growth boost could provide a tailwind for higher beta strategies such as US high yield. The Republican congress has already demonstrated its willingness to not curb spending so we believe the market should brace itself for significant volatility on the fiscal front in 2025.

Meanwhile, US protectionism, China slowdown and growth forecasts below trend may make it a difficult environment for emerging markets. We still believe there are ample opportunities across the different regions within emerging markets, especially in investment grade. Security selection, as ever, remains a critical component in this asset class.

Are net zero objectives worth pursuing?

Investment in the green transition should remain a major theme globally, even in the US, where the Trump administration has already started to unwind some of the support that the Biden administration provided. In particular, renewable energy and electric vehicle technology should continue to gain traction in 2025 mainly driven by demand from, and production in, emerging markets. The rapid increase in electricity demand from artificial intelligence related data centres will be met by an extension of renewable energy generation and upgrades to power grids. Hence, utilities and suppliers of technologies to support transmission should benefit.

For investors looking to reflect net zero objectives in their fixed income portfolios, there are two main ways to do this: carbon transition strategies and green bonds.

Carbon transition strategies allow investors to move from commitment and high-level target setting to concrete action within an investment portfolio to support the transition to a lower carbon economy.

Green bonds finance projects that have specific environmental objectives with the added benefit of transparent KPIs to monitor the progress of these green initiatives.

Subscribe to updates

Have our latest insights delivered straight to your inbox

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.