UK Outlook – Gradual easing in 2025 but lags will keep BoE cutting in 2026

- 04 December 2024 (5 min read)

KEY POINTS

The UK economy recovered strongly in the first half of 2024 after a technical recession in late 2023. But momentum fell back to trend in the second half of the year, as exceptionalism faded, uncertainty rose in the run-up to the Budget and yields rose. We see growth accelerating into 2025, largely on the back of policy support with the Budget underpinning around a 4% rise in government consumption next year. In contrast, the recovery in household spending looks set to remain sluggish, with the saving rate likely to remain well above pre-pandemic norms. Unlike the Office for Budget Responsibility (OBR), we see few reasons to expect a marked acceleration in spending, with the Budget re-enforcing our view the Bank of England (BoE) will reduce interest rates only gradually. This, along with the hike in employer National Insurance contributions (NICs), is likely to weigh on wage growth and employment. A degree of scarring is probably also keeping households cautious, given the size of the shocks experienced since the turn of the decade.

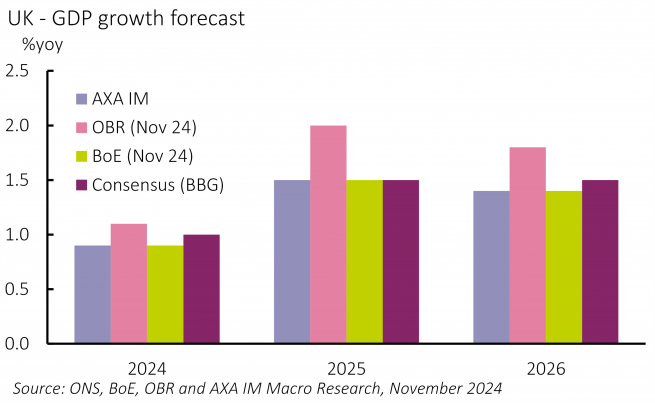

We see growth rising to 1.5% in 2025, well below the OBR’s 2.0% forecast (Exhibit 9). Further ahead, with public spending growth easing in 2026 and private spending likely to offset only part of that, we expect growth to slow to 1.4%. If growth comes in below the OBR’s forecasts, as we anticipate, the government is likely to be forced to increase either borrowing or taxes again in 2026, to cover the shortfall in tax receipts.

The recent surge in net migration will ease in 2025 and 2026, due to stricter policies, causing labour supply growth to ease. But labour demand will be modest at best; private sector firms already have enough staff to respond to a modest pick-up in demand, as the tight labour market reduced staff turnover recently. We see the unemployment rate rising to 4.5% by end-2025 and 4.6% by end-2026. As such, wage growth looks set to slow; we look for growth of 3.7% in 2025 and 3.3% in 2026. Note the 6.7% National Living Wage hike in spring 2025 will have a marginal impact as low-pay firms, such as Amazon and most major supermarkets, already pay above the National Living Wage and are less likely to pass on the full hike than in 2024, given the softer labour market.

CPI inflation, meanwhile, fell back to target midway through 2024 but a smaller drag from energy prices pushed it back up in October, and we see it rising to 2.5% by year-end. The headline rate will likely remain around this level throughout 2025, averaging 2.5% for the year. Tax changes outlined in the recent Budget – including the VAT on school fees and alcohol and tobacco duties – should add around 10 basis points (bp) to the outlook, while indirect impacts from the additional fiscal announcements, possibly including the pass through from higher employer NICS, will add to price pressures. We see inflation slowing to 2.2% in 2026, as the impact from the Budget eases and labour market conditions continue to soften, pushing down on wage growth and possibly profit margins.

The BoE cut its key policy rate at its August and November meetings, leaving Bank Rate at 4.75%. We think it will maintain this pace of easing throughout 2025, in line with its belief the UK economy requires a degree of economic slack to normalise pay and price-setting dynamics fully. Stronger-than-expected growth and inflation following the Budget and uncertainty surrounding how firms will handle the rise in employer NICs – firms could either raise prices, limit wage hikes, reduce employment or absorb the costs – means the BoE is keen to take time to see how these factors play out.

On balance, we forecast four 25bp cuts in 2025 – one per quarter – leaving Bank Rate at 3.75% by year end. In 2026, modest consumption growth will likely lead to excess supply opening up earlier than the BoE anticipates, exacerbated by our expectation of a material slowdown in the US. As a result, we think there is scope for additional cuts in 2026, whereas the market has Bank Rate broadly flat from the end of next year; we look for one additional cut in Q1, leaving Bank Rate at 3.5%.

Subscribe to updates

Have our latest insights delivered straight to your inbox.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.