UK reaction: Looser labour market conditions point to further cut

- 15 October 2024 (3 min read)

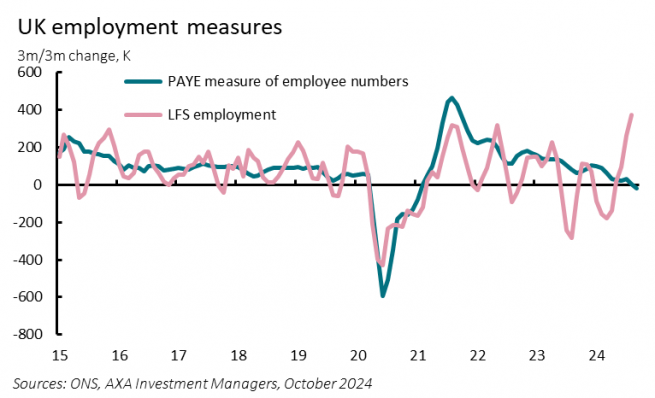

The latest labour market data point to an additional cut at the Bank of England’s meeting in November. The Labour Force Survey data showed a chunky 373K increase in employment in the three months to August and the unemployment rate edged down again to 4.0%, lower than in the previous three months and the level this time last year. Ongoing sampling issues, however, mean the data are unreliable and should be taken with a large pinch of salt. Note the survey reached an average of 88.5K individuals with a response rate to 42.8% (around 38k respondents), whereas in H1 2024, those figures were 53.1K and 17.6% (around 9k respondents), respectively.

Other measures continue to point to looser conditions. The number of vacancies, for instance, fell for the 27th consecutive period in the three months to September. And the PAYE measure of employee numbers was broadly unchanged in September – it fell by 15K on the month – after a drop of 35K in August, the largest since the early stages of the pandemic. The ONS also noted that year-over-year growth in both the Workforce Jobs – a measure based on business surveys – and the PAYE measures has slowed significantly over the past 18 months or so. The KPMG/REC Report on Jobs survey, meanwhile, suggested that some firms were putting hiring decisions on pause until after the Budget on October 30th, due to concerns over potential tax changes.

Likely most important for the BoE, though, will be the ongoing deceleration in wage growth. Average weekly earnings ex. bonuses fell to 4.9% - its slowest pace since June 2022 – from 5.1% in the three months to July, driven by declines in both public and private sector pay regular pay; the former slowed to 5.2%, from 5.7%, and the latter to 4.8%, from 5%. Total earnings – which include bonuses – fell further to 3.8% - over a three-and-a-half-year low - from 4.1%, though the disparity largely reflected base effects, given NHS workers and civil service workers were given one-off bonus payments across the summer in 2023. On a 3-m annualised basis, total earnings grew by 2.7% and ex-bonus payments by 4.4%.

On balance, the latest labour market data should convince a majority of MPC members in November that enough slack is developing to support a gradual deceleration in wage growth back to more sustainable levels over the next year or so. Note the BoE’s Decision Maker Panel survey showing businesses expect wage growth to be around 4% in 12 months’ time. In addition, we expect a renewed decline in CPI inflation in September – released tomorrow morning – to 1.8%, with services CPI inflation slowing to 5.1%. Both point to one further cut in Bank Rate in November. Further ahead, the key risk remains the Budget; if the Chancellor tightens fiscal policy materially in order to close the so-called fiscal “black hole” then the BoE may be forced to tighten more aggressively to offset the hit to growth.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© AXA Investment Managers 2024. All rights reserved

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.