Global Strategic bonds: A global approach to the new bond regime

As a new normal for government bond yields looks set to emerge, Nick Hayes, portfolio manager for our global strategic bonds strategy, outlines why this new regime is good news for unconstrained global fixed income.

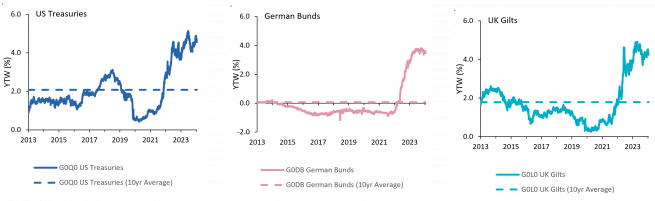

A return to the low-inflation, low central bank interest rate environment of the last decade looks unlikely. Underpinned by peak globalisation, large government bond supply, the energy transition and heightened geopolitical tensions a new era is emerging, where global inflation and government bond yields settle but remain elevated.

Changing risks, new opportunities

This new regime brings new market characteristics that shift the risks and opportunities for bond investors. Being aware of these changes means there is opportunity to enhance returns for global bond portfolios.

Fixed income yields have risen sharply in recent years, and this brings a compelling prospect for both attractive carry and capital gains. Furthermore, a higher-yielding environment gives the asset class a more favourable risk reward profile – the short- and longer-term outlook for fixed income is more attractive than it has been for some time.

The price for higher yields seems to be more volatility across global fixed income markets. We think that the unstable geopolitical backdrop, deglobalisation, shifting rate expectations, slower economic growth and the impact of tighter monetary policy is likely to see volatility continue.

But more volatility means more opportunities to find pockets of value within the global fixed income universe. Investors with a global view – and the necessary resources and expertise – can diversify holdings to insulate portfolios from large swings in local markets.

Diverging central bank policy presents tactical opportunities

While expectations of global rate cuts have been dialled back, we believe that central banks on this side of the Atlantic won’t wait for the Fed to cut first, and several emerging markets have already started cutting rates. This divergence brings opportunities for global bond portfolios, particularly for investors who can tactically manage their duration risk across different government bond curves.

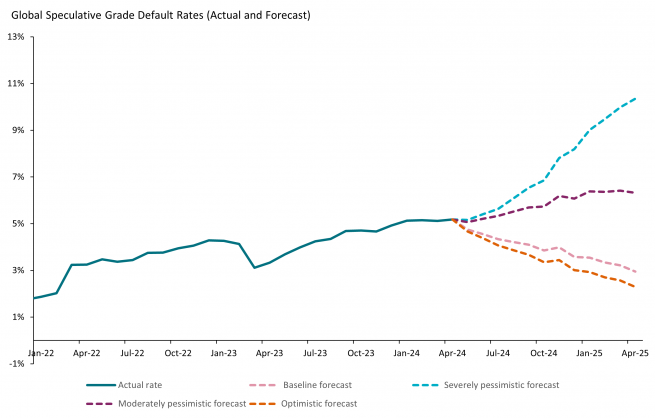

The lag effect of monetary policy is clearly affecting individual issuers and there has been a modest uptick in credit events. Default rates in global speculative-grade– one of the stronger performers of the global fixed income universe – have crept up from below 2.0.% two years ago to over 5.1%. We don’t believe that this indicates increasing systemic risk, but investors need to ensure that allocations to risk assets are backed up by rigorous bottom-up fundamental analysis to avoid being caught by defaults.

Positioning for the new regime

Positive on rates and credit

To make the most of different opportunities on either side of the Atlantic, our strategy is bar-belled across duration risk in Europe and lower quality credit in the US and emerging market debt.

Setting duration levels according to market divergence

We have been selling investment grade credit and using the proceeds to allocate further down the credit curve into US high yield and emerging market debt and to tactically manage our duration exposure, currently 4.8 years (as of 22 May 2024).

In line with our views on market divergence, we have been tactically choosing where to take duration risk, reducing dollar duration, but adding to European and UK curves. Our exposure currently stands at 3.5 years across UK and Europe and 1.3 years in the US.

Taking on risk

In credit, we prefer to take risk further down the credit spectrum. Despite strong spreads and rallies in recent times, all in yields remain attractive and company fundamentals remain strong, combined with healthy demand, should see spreads grind tighter and returns continue their recent positive trend.

Increasing allocation to emerging markets

We’re also more positive on emerging market corporates and sovereigns than we have been for some time. We believe there is an improving trend in some of the key restructuring stories of the last few years – Argentina, Gabon, Egypt and El Salvador are all names we own and are stand out recovery stories in their own right. While emerging market investment grade spreads are tighter than they have been for many years, it has been the compression of lower-rated names that has positively contributed.

Outperforming the global fixed income universe

In terms of the risk buckets that we use to organise our allocation, we have been increasing allocation to the aggressive category (High Yield Credit and Emerging Market Debt) and maintaining a third of our assets within the defensive category (Developed Market Government Bonds). This has been achieved at the expensive of intermediate assets (Investment Grade Credit and Periphery Government), where the proceeds from investment grade credit have been used to buy credit further down the risk spectrum and to tactically manage our duration exposure.

Source: AXA IM as of 30 April 2024. Risk Bucket historic high, low and current allocation. Based on month end positions since inception (19/10/2020)

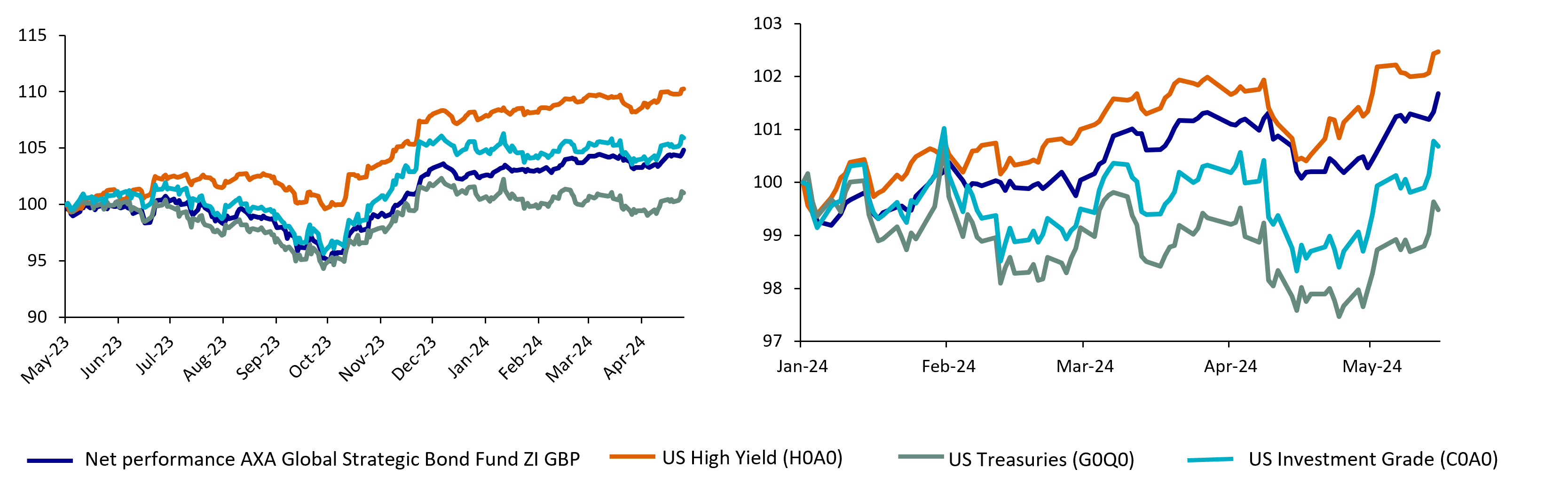

In this new regime we are seeing some volatility in the performance of individual fixed income asset classes where one month’s performance can quickly be eroded by the next. By maintaining structural diversification across fixed income risk factors, tactically managing where and when to add duration and having conviction in single names means over the past year and year to date periods our strategy has captured the upside when markets have rallied and avoided the worst of the volatility when markets have trended sideways.

Source: AXA IM as of 16 May 2024.

Our recent performance demonstrates the strong momentum building in our strategy, while our longer-term track record highlights the ability to deliver in a variety of market conditions. We are confident that we have the expertise and right investment framework and philosophy to deliver risk adjusted fixed income returns in the new market environment we are facing.

Important Information

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional or Wholesale Clients / Investors only, as defined by applicable local laws and regulation.

Circulation must be restricted accordingly.

Capital at risk. The value of investments, and any income from them, can fall as well as rise and investors may not get back the amount originally invested.

Additional risks

Counterparty Risk: failure by any counterparty to a transaction (e.g. derivatives) with the Fund to meet its obligations may adversely affect the value of the Fund. The Fund may receive assets from the counterparty to protect against any such adverse effect but there is a risk that the value of such assets at the time of the failure would be insufficient to cover the loss to the Fund.

Derivatives: derivatives can be more volatile than the underlying asset and may result in greater fluctuations to the Fund's value. In the case of derivatives not traded on an exchange they may be subject to additional counterparty and liquidity risk.

Interest Rate Risk: fluctuations in interest rates will change the value of bonds, impacting the value of the Fund. Generally, when interest rates rise, the value of the bonds fall and vice versa. The valuation of bonds will also change according to market perceptions of future movements in interest rates.

Emerging Market Risks: emerging markets or less developed countries may face more political, economic or structural challenges than developed countries. As a result, investments in such countries may cause greater fluctuations in the Fund's value than investments in more developed countries.

Liquidity Risk: some investments may trade infrequently and in small volumes. As a result, the fund manager may not be able to sell at a preferred time or volume or at a price close to the last quoted valuation. The fund manager may be forced to sell a number of such investments as a result of a large redemption of shares in the Fund. Depending on market conditions, this could lead to a significant drop in the Fund's value and in extreme circumstances lead the Fund to be unable to meet its redemptions.

Credit Risk: the risk that an issuer of bonds will default on its obligations to pay income or repay capital, resulting in a decrease in Fund value. The value of a bond (and, subsequently, the Fund) is also affected by changes in market perceptions of the risk of future default. The risk of default for high yield bonds may be greater.

Risks linked to investment in sovereign debt: Where bonds are issued by countries and governments (sovereign debt), the governmental entity that controls the repayment of sovereign debt may not be able or willing to repay the capital and/or interest when due in accordance with the terms of such debt. In the event of a default of the sovereign issuer, a Fund may suffer significant loss.

High yield bonds risk: These bonds are issued by companies or governments with lower credit ratings and as such are at greater risk of default or rating downgrades than investment grade bonds.

The fund is also subject to geopolitical risk, securitised assets or CDO assets risk and contingent convertible bonds (“CoCos”).

Further explanation of the risks associated with an investment in this strategy can be found in the prospectus.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Before making an investment, investors should read the relevant Prospectus and the Key Investor Information Document / scheme documents, which provide full product details including investment charges and risks. The information contained herein is not a substitute for those documents or for professional external advice.

The products or strategies discussed in this document may not be registered nor available in your jurisdiction. Please check the countries of registration with the asset manager, or on the web site https://www.axa-im.com/en/registration-map, where a fund registration map is available. In particular units of the funds may not be offered, sold or delivered to U.S. Persons within the meaning of Regulation S of the U.S. Securities Act of 1933. The tax treatment relating to the holding, acquisition or disposal of shares or units in the fund depends on each investor’s tax status or treatment and may be subject to change. Any potential investor is strongly encouraged to seek advice from its own tax advisors.

For more information on sustainability-related aspects please visit https://www.axa-im.com/what-is-sfdr

For investors located in the European Union:

Please note that the management company reserves the right, at any time, to no longer market the product(s) mentioned in this communication in the European Union by filing a notification to its supervision authority, in accordance with European passport rules.

In the event of dissatisfaction with AXA Investment Managers products or services, you have the right to make a complaint, either with the marketer or directly with the management company (more information on AXA IM complaints policy is available in English: https://www.axa-im.com/important-information/comments-and-complaints ). If you reside in one of the European Union countries, you also have the right to take legal or extra-judicial action at any time. The European online dispute resolution platform allows you to submit a complaint form (available at: https://ec.europa.eu/consumers/odr/main/index.cfm?event=main.home.chooseLanguage) and provides you with information on available means of redress (available at: https://ec.europa.eu/consumers/odr/main/?event=main.adr.show2).

Summary of investor rights in English is available on AXA IM website https://www.axa-im.com/important-information/summary-investor-rights. Translations into other languages are available on local AXA IM entities’ websites.

AXA Global Strategic Bond Fund is a sub-fund of AXA IM Fixed Income Investment Strategies which is a Luxembourg UCITS Fund (“fonds commun de placement”) approved by the CSSF. It is managed by AXA Investment Managers Paris , a company incorporated under the laws of France, having its registered office located at Tour Majunga– La Défense 9 – 6, place de la Pyramide,– 92800 Puteaux, registered with the Nanterre Trade and Companies Register under number 353 534 506, and a Portfolio Management Company, holder of AMF approval no. GP 92008, issued on 7 April 1992.

Past performance is not a guide to current or future performance, and any performance or return data displayed does not take into account commissions and costs incurred when issuing or redeeming units. References to league tables and awards are not an indicator of future performance or places in league tables or awards and should not be construed as an endorsement of any AXA IM company or their products or services. Please refer to the websites of the sponsors/issuers for information regarding the criteria on which the awards/ratings are based. The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested. Exchange-rate fluctuations may also affect the value of their investment. Due to this and the initial charge that is usually made, an investment is not usually suitable as a short term holding.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.