Using short duration as a liquidity tool

KEY POINTS

For investors with large cash balances following the recent period of high interest rates, it may be time to start considering how the liquid allocation within their portfolio is positioned with rate cuts on the horizon. There is a case for considering short duration bonds for those investors looking to enhance performance of their liquidity portfolios while mitigating risk.

Short-dated bonds – A compelling alternative to enhance cash returns

Short-dated bonds typically have maturities up to five years, making them a potentially suitable bridge between cash holdings and longer-term fixed income investments. While riskier than cash, the higher returns on offer, limited volatility and natural liquidity of short-dated bonds should make them an attractive consideration for the liquid part of an investor’s portfolio.

There are key characteristics of short-dated bonds that make them particularly suited for liquidity management.

- Low volatility: Short-dated bonds tend to exhibit much lower price volatility compared to their longer-term counterparts, making them an attractive option for cash liquidity strategies.

- Natural liquidity pipeline: As short-dated bonds mature, the principal is returned to the investor, creating a natural liquidity pipeline. This reduces the need to trade and incur additional costs, further benefiting portfolio performance.

- Pull to Par: In environments where bonds are trading at a discount, the pull to par opportunity – where bonds are redeemed at their face value upon maturity – is attractive. This can potentially enhance returns, even when central bank rates are rising.

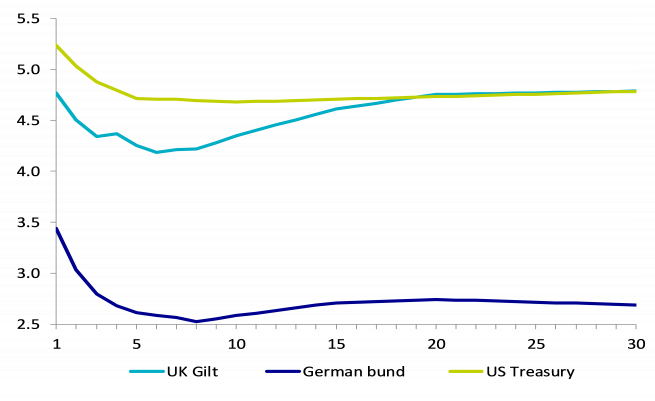

Reasons for short duration

The inversion of sovereign yield curves, flat credit curves and continuing attractive yield valuations mean we continue to see opportunities in short duration strategies. As shown in the chart below, by investing in short duration strategies you should be able to minimise your duration risk while maximising your yield.

Short-dated bonds have proven their resilience over this hiking cycle, providing much better returns when compared to longer duration strategies. As we’ve now reached the peak of this hiking cycle, central banks may start cutting interest rates which should lead to falling cash rates. As such, there is an opportunity cost to remaining heavily invested in cash as short-dated bonds should outperform it by benefitting from the fall in sovereign yields on the back of lower interest rates.

Moreover, opting for active management offers additional advantages such as default risk mitigation, avoiding forced sales, and the potential for yield enhancement through careful bond selection. By considering short-dated bonds as part of a cash liquidity strategy rather than a traditional bond allocation, it may help investors optimise their portfolios and navigate the complexities of the current financial landscape.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Risk warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.