Emerging Markets Outlook – Resilience to be tested

- 04 December 2024 (5 min read)

KEY POINTS

Emerging markets (EMs) likely face a deteriorating external environment in 2025-2026, which will further test their resilience. EMs withstood a series of shocks over the past five years - the pandemic, an inflationary surge and 2022’s terms-of-trade shock (higher energy and food prices). The prospect of greater US trade protectionism during Donald Trump’s second term, as well as continued challenges facing China’s policymakers in reviving their sluggish economy, present downside risks to EM economic growth. We see risks on the downside for oil prices – reflecting increased supply, Trump’s deregulation agenda and global growth deceleration – but geopolitical tail risks in the Middle East could trigger a temporary spike in oil prices. Trump has pledged to end the Ukraine war but the terms of a resolution could have consequences for security arrangements for EM Europe, requiring an expansion in defence spending at a time when debt ratios and interest rate payments are elevated.

Against this backdrop, policymakers across EMs will continue to need to deliberate over decisions that prepare for, or react to, changes beyond their control, while adjusting monetary and fiscal policy to support domestic demand without risking a reacceleration in inflation or generating fiscal crises.

Numerous new governments have been formed over the past year across EMs and this provides the opportunity for meaningful reform agendas to be implemented. But success in driving up investment will be as much about avoiding policy mistakes as it will be about delivering structural reforms to improve competitiveness and productivity.

Back on an even keel but choppy waters ahead

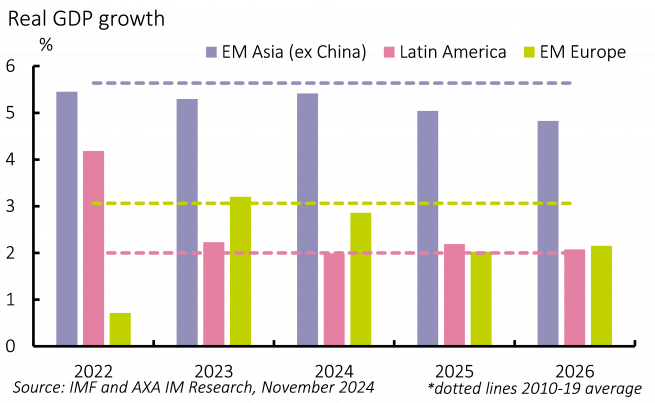

EMs have enjoyed broad success in terms of getting economic growth back on trend in the past year while containing inflation. However, the EM growth path could yet shift dramatically off course as external headwinds ramp up.

The top-line forecast for growth in 2025-2026 reflects an expectation that the pace of expansion in EMs will maintain a degree of resilience in the face of external challenges (Exhibit 14). This will mostly be reliant on private consumption growth, with recent cuts in interest rates and sizeable real income gains (reflecting disinflation and resilient labour markets) providing some scope for increased spending in 2025. However, room for further monetary easing or fiscal loosening is limited. Investment growth will be hindered by heightened uncertainty over US trade policy. Although it may take time for tariffs to be enforced and the direct impact to the registered, the indirect impact on investment will be evident heading into 2025, as plans are potentially delayed or put on hold until a clearer picture emerges on Trump’s policies.

Our central scenario is one of US tariffs being introduced at around one-third of the promised magnitude of 60% on China and 10% on all other imports. But even at this level, higher tariffs will weigh heavily on EM export performance, with the larger open economies struggling to expand at trend level – with risks of a broader trade war. The larger domestic-oriented economies, such as India and Indonesia, should fare better but any major disruption to global trade and capital markets will still have an impact.

There will be idiosyncrasies that will generate positive growth outcomes in some markets, offsetting weakness elsewhere. Argentina, for example, could post growth of close to 5% a year in 2025-2026 as its economy recovers from the contraction recorded in the past two years, provided the stabilisation programme is not derailed. Colombia’s GDP growth is also expected to accelerate from 2024’s lows as its domestic demand heals thanks to an easing from very tight domestic financial conditions. That will prop up the regional average, despite anticipation of growth deceleration in Brazil and Mexico. Turkey’s economic growth is also set to pick up in 2026 on the basis that the benefits of the current orthodox monetary policy will be reaped, with massive interest rate cuts expected in 2025 underpinning a rebound in growth in 2026.

EMs caught in tariff crossfire

Trump’s resounding success in the US presidential election gives him a solid platform to deliver on his “America First” policies by hiking tariffs as soon as he takes office. China will face the brunt of this protectionism, with 60% tariffs threatened, but a proposed blanket 10% tariff on all US imports would have a far-reaching impact on EMs. However, higher tariffs on China’s goods could potentially benefit its competitors, particularly manufacturers in EM Asia that have struggled to compete with China on price. Yet any benefit will depend on the extent of the likely yuan depreciation.

Although China’s significance as an export destination for EMs has been limited recently by weak domestic demand, China still accounts for a large share of many EM exports, such as for Chile (39% of its exports in 2023), Brazil (31%) and Indonesia (22%). Much of this comprises commodities and raw materials as well as intermediate goods that ultimately feed into Chinese industrial production and manufacturing exports. Thus, any constraints on China’s exports will negatively hit EM suppliers.

To compensate for any shrinkage in US demand following a potential hike in tariffs, Chinese exporters could redirect these goods to other markets. Fearing a surge in low-cost Chinese imports undermining the competitiveness of domestic suppliers, EMs could attempt to erect new, or raise existing, trade barriers to China. Indonesia has already taken such steps. But this risks retaliatory measures from China, which accounts for a relatively large share of EM imports and increasing foreign direct investment (FDI) flows into South-East Asia.

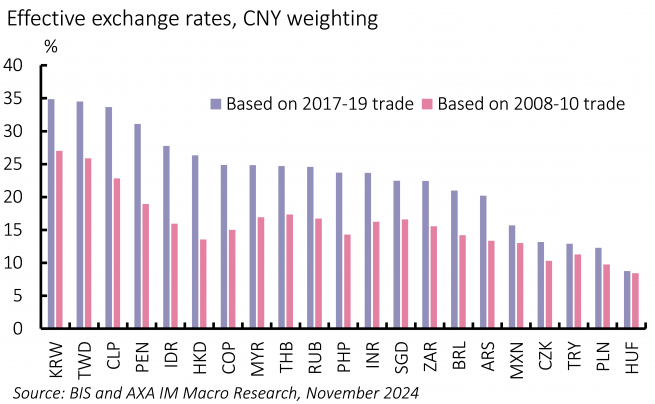

With the prospect of further yuan devaluation compounding these potential changes in EM-China trade dynamics, EM currencies are also likely to come under broader pressure, which would increase the vulnerability of those reliant on imports or with significant US dollar debt. The yuan now accounts for a much greater weight in the currency baskets for EMs’ effective exchange rate indices (Exhibit 15).

Supply chain rewiring supports investment in EM

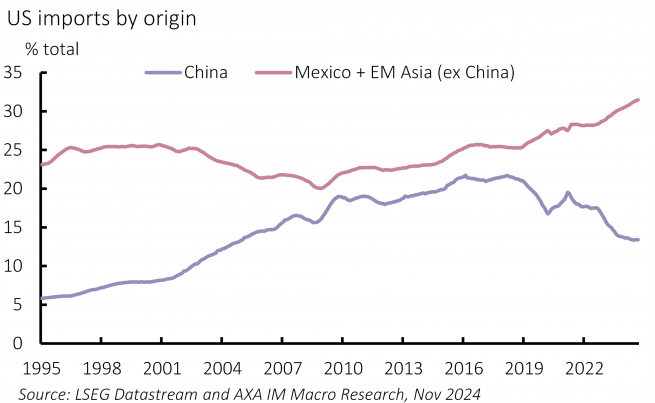

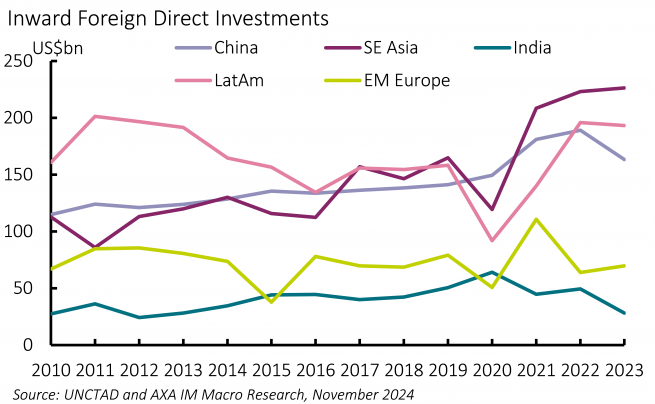

Since the start of the US-China trade war during Trump’s first term, there has been a major reconfiguration in supply chains delivering goods to the US. In early 2018, China accounted for close to 22% of US imports, but by mid-2024 its share had dropped to 13% (Exhibit 16). Other EMs have replaced China, notably South-East Asian markets, such as Vietnam and Malaysia, as well as Mexico. Other factors have also been at play, but a key contribution to this shift has been the rerouting of Chinese goods via these other markets. Initially, this may have taken the form of minimal additional processing by manufacturers and traders in these markets, but more recently the supply chain rewiring also reflects a shift of Chinese manufacturing capacity into these markets. This has also been taking place in EM Europe, where China’s investment in electric vehicle (EV) manufacturing in Hungary, for example, has come at a time of EU tariff hikes. Moreover, an increase in total FDI to South-East Asia and Latin America, while that to China has fallen, is a broad indicator of how investment has shifted away from China to EMs as part of ‘China+1’ strategies. This could find renewed impetus with Trump’s plan to hike tariffs on exports out of China.

However, there will be a wariness in US trade policy cracking down on any circumvention of its tariffs. This has already been the case under President Joe Biden. In August 2023, a US Department of Commerce inquiry found Chinese producers were shipping solar products through South-East Asian markets for minor processing to avoid paying anti-dumping and countervailing duties.

Trump may not concern himself with such inquiries before imposing hefty penalties. When campaigning, he stated he would impose a 100% tariff on Chinese-produced EVs from Mexico, despite the US-Mexico-Canada Agreement (USMCA) trade deal. The USMCA is up for review in July 2026, and this will no doubt have a focus on dealing with China’s investment in Mexico. Ahead of this, Trump will likely use threats of tariffs and a tougher trade deal to secure a favourable outcome for his administration on its China and immigration policies.

Others that have seen trade surpluses with the US widen in recent years also face the risk of a protectionist response from Trump. This is most pronounced for South Korea and Taiwan, which continue to drive technology exports, with strong demand for semiconductors as investment in artificial intelligence (AI) continues on an upward trend. There is also a security element to US relations with Taiwan and Korea. A harbinger of more complicated US-Taiwan relations was Trump’s comments in July that Taiwan should pay the US for protection from China, while also bemoaning Taiwan’s dominance in the global semiconductor trade. Meanwhile in his first term, Trump accused South Korea of free-riding on US security support (in relation to North Korea) and renegotiated the Korea-US Free Trade Agreement.

EM central banks more cautious on rate cutting

Irrespective of the US election outcome, EMs were already facing the prospect of a slowdown in the US, Eurozone and China. Following Trump’s election victory, our central scenario sees US growth slow to 2.3% in 2025 and 1.5% in 2026 from 2.8% in 2024, while China’s GDP growth is forecast to decelerate to 4.5% and 4.1% respectively in 2025 and 2026, from 4.8% in 2024. The Eurozone will likely remain sluggish, with growth rising to just over 1% in 2025-2026. Given this weak external environment, EM domestic demand will need a boost. Private consumption growth has stayed above pre-pandemic rates for most EMs but its contribution to overall GDP growth across EMs has been falling back steadily from the post-pandemic recovery highs. Given the weaker external environment, the challenges for policymakers will be to utilise fiscal and monetary tools to deliver support for their domestic economies without risking renewed inflationary pressure or worsening fiscal positions to the point of raising investor concerns over debt-servicing risks.

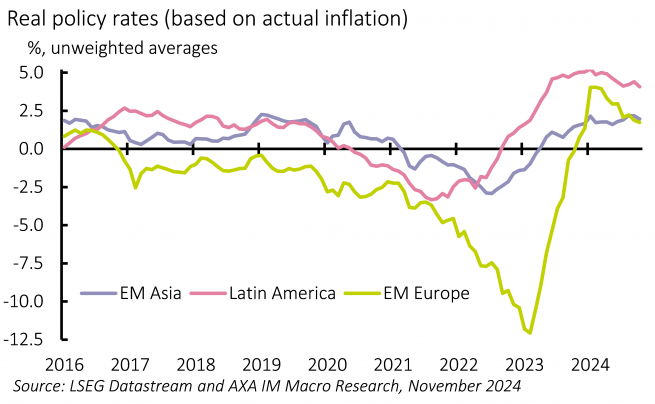

With inflation generally falling back to – or closer to – target, most EM central banks have been cutting rates (with the notable exception of Brazil) and easing cycles are now well underway. Yet real rates based on short-run inflation expectations still stand well above estimated neutral rates in countries such as Mexico, Colombia, Brazil, South Africa, Hungary, Peru and the Czech Republic. The ‘last mile’ on inflation may still prove difficult for some key EMs in Latin America and Europe given sticky services inflation. But a less restrictive monetary policy stance is likely given slowing growth and inflation across most EMs (Exhibit 17).

But EM central banks will also be mindful of financial stability risks, including fiscal risks (which have led Brazil’s central bank to embark on a tightening cycle) and external risks. The inflationary impact of Trump’s tax, trade and immigration policies will make the Federal Reserve more cautious in cutting rates in 2025 and the US dollar remain strong. In turn, elevated US yields and a strong US dollar may delay monetary policy easing in EMs and keep the policy stance restrictive for longer. India is likely to be one of the last of the major EMs globally to start easing monetary policy as domestic demand proves resilient. The Reserve Bank of India’s decision at its October meeting to shift its liquidity stance to neutral from “removal of accommodation” foreshadows an eventual rate cut, but we expect it to stay focused on getting inflation down sustainably within target, which could mean a shallow rate cutting cycle.

Limited scope for fiscal loosening

Fiscal space is limited across EMs, with government debt ratios and borrowing costs having risen over recent years. At worst, attempts to deliver measures to stimulate demand may backfire, as wider deficits trigger debt sustainability concerns and force higher rates, with negative effects on growth and debt servicing capacity. As developments in Brazil highlight, the future path of monetary and fiscal policy is intertwined, with fiscal activism in Brazil driving up inflation expectations, leading an inflation-targeting central bank to hike rates. Similarly, in Mexico, the space for the central bank to continue its so far gradual monetary easing is contingent on the government’s success in bringing down its deficit. Mexico’s new government has planned to reduce the deficit to 3.9% of GDP in 2025, from an estimated 5.9% in 2024 but this is based on optimistic forecasts for growth and oil production.

With fiscal consolidation delayed, EMs have failed to regain fiscal space. This year was another disappointing period for fiscal discipline across EMs. The International Monetary Fund’s (IMF) recent Fiscal Monitor shows the cyclically-adjusted general government primary deficit for EMs in 2024 widened further by 0.1% to 3.6% of GDP, well above the 2.7% deficit in 2019. Rather than being primed to deliver fiscal support, EMs overall are focused on fiscal tightening in 2025 and 2026 to restore credibility. This is notable for Mexico and Turkey, where a large fiscal consolidation effort is expected. In Turkey, tolerance for lower growth will be key if macroeconomic stability is to be preserved, as fiscal policy needs to cooperate with monetary policy to achieve a sustained reduction in inflation. In Mexico, the planned fiscal tightening, mostly through spending cuts, will weigh on domestic demand and growth at a time of a deteriorating external environment.

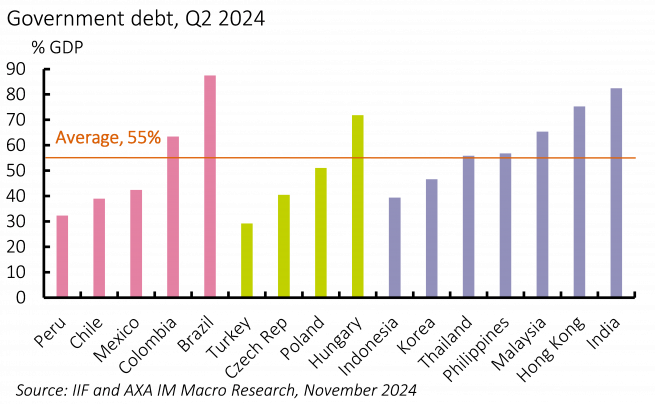

India’s deficit is on a gradual reduction path, but the combination of high government debt (82% of GDP as of mid-2024) and a wide deficit places it alongside Brazil as among the most debt-constrained large EMs (Exhibit 18). This may be less of a concern for India given its outlook for high nominal GDP growth, but Brazil is heading into a more challenging period. Although trend growth has improved, a marked improvement in Brazil’s primary fiscal position is necessary to start reducing its debt burden, an outcome that is challenging given the fast growth in mandatory expenses.

Thailand is one of the few EMs that has already planned to run a wider deficit in 2025, with the cyclically adjusted deficit set to increase to 3.9% of GDP in 2025 from 2.5% in 2024, according to the IMF. The Thai economy has been particularly weak since the pandemic, and the Prime Minister, Paetongtarn Shinawatra, who came to office in August 2024, is pushing through a spending programme featuring cash handouts to try to drive up consumption. Although Thailand’s government debt-to-GDP is not excessive (56% as of mid-2024), household debt is among the highest of EMs at 91% of GDP, which may limit the impact of fiscal stimulus.

Structural reforms bring rewards

Structural reform has not been high on the policy agenda since the pandemic, and given the forthcoming expansion in US protectionism, EM policymaking will continue to be impacted by external developments and changes beyond countries’ control. However, with only a small number of elections taking place in 2025-2026, and many new governments receiving new or extended multi-year mandates in 2024, there is scope for meaningful reform with a longer-term view.

A few ‘reform stories’ have developed over the course of 2024 and are likely to bolster growth dynamics over time. The new government in South Africa is undertaking energy and logistics reforms, set to improve the supply side of the economy and raise its trend growth. Egypt has embarked on a structural reform agenda, which includes subsidy reductions, tax reform, privatisation and a more flexible foreign exchange regime, aimed at combining macro and fiscal stabilisation with higher growth. In Nigeria, subsidy reform and a more flexible foreign exchange regime implemented by President Bola Tinubu’s administration since 2023 have started to bear fruit. In Argentina, President Javier Milei has liberalised product markets and implemented a sharp spending-based fiscal consolidation, which, together with a foreign exchange anchor, has driven a massive reduction in inflation and set the stage for activity to recover.

Reforms that started in the late 1990s have contributed to some of the EM resilience of recent years, with central bank independence, financial market openness and exchange rate flexibility providing key buffers. But some of the more challenging, and potentially unpopular reforms, notably in terms of land, labour markets and tax, have been left on the back burner. For example, India has struggled to attract higher levels of FDI in recent years, which in part reflects the broad challenges that persist when doing business in India (despite recent liberalisation efforts and corporate tax cuts), as well as a failure to proceed with agriculture and land reforms. However, markets that have made progress have mostly been rewarded. In Brazil, for example, the IMF has revised higher its trend growth to 2.5% from 2%, partly on the back of the past fiscal reform to simplify the sales tax system and the 2016 labour market reform.

Growth prospects in EMs are also reliant on stable political environments or at least an avoidance of moves that destabilise or create uncertainty. Hungary has made no progress this year in unblocking EU funds that are still withheld owing to concerns over the rule of law. Relations between Hungary and the EU remain contentious. The prime minister, Viktor Orbán, has been in power since 2010 and will not face the electorate again until April 2026, but recent opinion polls showed a new centre-right party, Tisza, had overtaken Orbán’s Fidesz, raising the risk of Orbán stepping up hardline anti-EU rhetoric. Hungary’s current recession is the result of weak demand from Germany, specialisation in the automotive sector and tight macroeconomics policies. However, weak governance that has prolonged the standoff with the EU has prevented Hungary from funding public investment and taking advantage of growth opportunities in areas such as the green economy.

In Latin America, Mexican President Claudia Sheinbaum, who won a landslide victory in the June 2024 elections, is proceeding with her predecessor’s judicial reforms (allowing judges to be elected by popular vote) and other constitutional reforms. These could dent the attraction of Mexico for foreign investment, jeopardise its ‘nearshoring’ potential and add to uncertainty in the scheduled USMCA review in 2026.

Reasons to be cheerful

A one-size-fits-all approach to assessing the outlook for EMs risks over-simplification but while few EMs will avoid the negative consequences of the worsening external environment, domestic demand resilience has improved and overall growth will broadly stay the course (albeit at a below trend rate for most EMs). There is clear downside risk in the event of Trump going all-out on his trade protection threats, or a broader trade war, but there are also still upside risks for EMs if his campaign pledges turn out to be little more than initial bargaining chips or if China makes progress in reflating its economy.

Among the positive EM growth stories is India, with its economy becoming more resilient over the past decade, and with Narendra Modi securing another five years in office in the 2024 elections, current investment-promoting policies should continue. This, combined with India’s growing consumer market, should keep annual growth above 6%. Indonesia is also primed for continued growth of around 5% a year. In terms of its fiscal dynamics (low deficit and low debt), Indonesia’s new government under Prabowo Subianto is relatively well-placed to take steps to support the economy, and spending on infrastructure and industrial policies aimed at driving up domestic value-add will continue.

Elsewhere in Asia, Korea and Taiwan have benefited from the boom in AI investment, with sales from their advanced semiconductor manufacturers driving a strong recovery in technology exports. While non-technology exports appear to be losing momentum, investment in AI is set to persist over the medium-term horizon, and this will have positive spillovers to technology manufacturers across the region.

There is also the potential for continued growth in EM FDI (Exhibit 19), as manufacturers continue to shift supply chains away from China to avoid potential future US and EU protectionist measures. Although this will draw the attention of the Trump administration (and the EU) if Chinese firms are involved, the more competitive EMs could thrive as supply chains continue to be reconfigured. Those less so will be encouraged to embark on pressing but challenging reforms to attract FDI.

Although not yet a positive growth story, Argentina’s ‘shock therapy’ reform agenda aims to unleash ‘animal spirits’ in the economy. Milei’s initial package was diluted given his party’s limited power in the legislature, but he has implemented structural reforms, including deregulation and labour market reform. Argentina will hold mid-term parliamentary elections in October 2025, which could provide a stronger footing for Milei to push forward with his reforms amid popular support that has remained surprisingly resilient so far.

Subscribe to updates

Have our latest insights delivered straight to your inbox.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.