Central bank digital currencies, reserve currencies and geopolitics

- 11 June 2021 (15 min read)

When it comes to central bank digital currencies (CBDCs), the focus of market participants and regulators – especially in the banking industry - is mainly associated with their disruptive nature. Instead, we focus this analysis on their geo-strategic implications, including for the business of offering and accumulating foreign exchange reserves.

The impact of CBDCs on reserve currencies

The International Monetary Fund (IMF) defines foreign exchange reserves as “official public sector foreign assets that are readily available to and controlled by the monetary authorities”1 . A broader definition also includes the objective and the best practice of reserve management: “(i) adequate foreign exchange reserves are available for meeting a defined range of objectives; (ii) liquidity, market, and credit risks are controlled in a prudent manner; and (iii) subject to liquidity and other risk constraints, reasonable earnings are generated over the medium to long term on the funds invested.”1

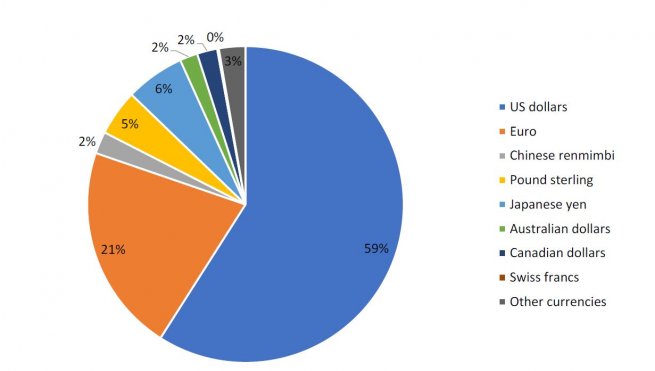

Would a digital currency, or more generally a digital asset, qualify as a reserve currency/asset? So far, only a very limited subset of the existing asset universe enjoys reserve status. Worldwide allocated reserves amounted to $11.9trn at the end of 2020, of which roughly 80% were denominated in either US dollars or euros (Exhibit 1). Furthermore, the majority of foreign reserves is invested in government bonds with a relatively contained maturity.

- SU1GICgyMDAxKSwgR3VpZGVsaW5lcyBmb3IgRm9yZWlnbiBFeGNoYW5nZSBSZXNlcnZlIE1hbmFnZW1lbnQ=

- SU1GICgyMDAxKSwgR3VpZGVsaW5lcyBmb3IgRm9yZWlnbiBFeGNoYW5nZSBSZXNlcnZlIE1hbmFnZW1lbnQ=

To tackle the question about reserve currency status, it might be worth taking a step back to recall the functions of money:

- Medium of exchange/payment;

- Measure of value: Prices are expressed in predefined units (so-called numeraire, e.g. dollars); and

- Store of value: Money needs to retain its value in time, otherwise firms and households will search for better alternatives.

Ideally, money is a fungible, durable, portable and identifiable medium with a stable value. To put it bluntly: “Money is the most universal and most efficient system of mutual trust ever devised…even people who do not believe in the same god or obey the same king are more than willing to use the same money.”2

Another characteristic of money, equally important and innovative in our view, is related to information: “We assume that money is also a store of information. As currency is a disseminator of information, individuals consider the privacy (transparency) risks inherent in using a given currency for trading, given that any exchange can disseminate information on the exchangers. In other words, we assume the existence of expected privacy costs – or anonymity costs – when using money for exchanges. These privacy costs can be associated with the value of each transaction and with the number of transactions.”3

Central bank digital currency4 is a natural evolution of existing forms of money (for example cash or sight deposits), which actually satisfies all four characteristics of money described above. CBDCs have the ability to maximise this fourth function, perhaps at the cost of privacy. Other means of payment, such as crypto assets and stablecoins, might tick some of the boxes as well, but not all (Exhibit 2). Therefore, we regard them as instruments that are inferior to CBDC in the context of reserves management and deem them at risk of being crowded out by CBDCs.

- SGFyYXJpICgyMDE1KSwgU2FwaWVuczogQSBCcmllZiBIaXN0b3J5IG9mIEh1bWFua2luZCwgSGFycGVy

- TWFzY2lhbmRhcm8gKDIwMTgpLCBDZW50cmFsIEJhbmsgRGlnaXRhbCBDYXNoIGFuZCBDcnlwdG9jdXJyZW5jaWVzOiBJbnNpZ2h0cyBmcm9tIGEgQmF1bW9sLUZyaWVkbWFuIERlbWFuZCBmb3IgTW9uZXksIGRyYWZ0LCBCb2Njb25pIFVuaXZlcnNpdHk=

- VGVudG9yaSAoMjAyMSksIENlbnRyYWwgQmFuayBEaWdpdGFsIEN1cnJlbmN5OiBQb2xpY3kgYW5kIERlc2lnbiwgQVhBIEludmVzdG1lbnQgTWFuYWdlcnM=

We can further refine the distinction between the various forms of digital means of payment by using the “money tree” approach proposed by the IMF5 :

- Type of payment: Claim versus object;

- Value of payment: Fixed versus variable redemption value (for claims) and denomination (for objects);

- Redemption guarantee (for claims only): Private versus government backstop; and

- Technology: Centralised versus decentralised settlement.

While it seems pretty uncontroversial that crypto assets cannot be efficient and effective units of account and means of payment, a question mark exists on whether they can still represent a store of value. There are arguments in favour of, and against, this assertion.

The arguments in favour are:

- As long as they are – or perceived to be – scarce, and their users believe that they have a value, they will have a value;

- In a world in which currencies will also have an additional function, i.e. carrying information about the transactions, anonymity may have an intrinsic value;

- If crypto assets are used as collateral for traditional transactions like mortgages, then their value could be greatly enhanced by positive network effects – although the risk is that of creating a house of cards;

- Even if the value of the underlying asset may be negligible, the value of the institutions created to trade it may be very attractive. For example Coinbase, a trading platform for crypto assets, recently listed on NASDAQ and saw its share price surge before the first day of trading6 , though the price later fell; and

- If traditional means of payments (such as PayPal and Visa) start accepting payments in bitcoins and other crypto assets, their value may increase as they may be perceived as future means of payments.

The arguments against are:

- Crypto assets do not have physical or intrinsic value;

- They don’t have value of use, unlike gold or other precious metals;

- They don’t produce returns, so their value cannot be determined by the discounted cash flow of future inflows;

- A track record of “forks” (changes in protocol that result in two branches) have severely reduced the concept of maximum amount available of crypto assets;

- They are not backed by assets such as gold, special drawing rights or government bonds; and

- The volatility of their valuations makes them unfit to be a stable store of value (Exhibit 3).

To summarise, at the moment it is too early to say whether crypto assets could be considered a store of value. But certainly the discussion is open and ongoing.

The backstop – a digital currency’s collateral framework – is key in order to distinguish so-called stablecoins from the broader ecology of digital currencies. It is an essential design feature, one likely to influence the path of adoption of any nascent digital currency. One could object that after the collapse of the gold standard, the value of traditional currencies is only implicitly backed by the sovereign (e.g. via tax revenues or net wealth). Credibility, trust and confidence are therefore essential features of traditional and digital currencies alike.

- QWRyaWFuL01hbmNpbmktR3JpZmZvbGkgKDIwMTkpLCBDZW50cmFsIEJhbmsgRGlnaXRhbCBDdXJyZW5jeTogNCBRdWVzdGlvbnMgYW5kIEFuc3dlcnMsIElNRiBCbG9n

- Q29pbmJhc2UgRmV0Y2hlcyAkODUgQmlsbGlvbiBWYWx1YXRpb24gaW4gTWFya2V0IERlYnV0IC0gV1NK

Exhibit 3 compares the realised volatility of bitcoin, gold and the euro/US dollar exchange rate. Needless to say, the euro satisfies its store-of-value requisites better than gold and bitcoin. A low volatility currency also better captures the confidence of its (potential) users. The broader idea is to limit excessive price swings typical of crypto assets so as to better align the digital currency with existing, traditional currencies. As former European Central Bank (ECB) Executive Board member Benoît Cœuré stated: “Originally envisioned as an accessible and borderless way to pay, crypto-assets have generally suffered from severe price volatility and limited capacity to process transactions compared with existing arrangements… The developers of the crypto-assets labelled ‘stablecoins’ seek to reduce volatility by anchoring the ‘coin’ to a reference asset (e.g. a sovereign currency) or a basket of assets.”7

We’ve established that designs like stablecoin and CBDC are superior to crypto assets, at least from the viewpoint of a reserve manager. Still, we’re left with the important question of timing. In particular, there seems to be an unusually large gap between major central banks’ timeline for the introduction of CBDCs. After a relatively short period of scepticism, central bankers are now collectively studying and experimenting with digital currencies.

According to the Bank for International Settlements (BIS)8 , roughly 80% of the world’s central banks are currently engaging in CBDC research, experimentation and development. Moreover, 20% of the world’s central banks are planning to launch a retail CBDC in the medium term. The ECB has recently released a comprehensive report on a digital euro9 and the US Federal Reserve (Fed) has launched a CBDC project together with the Massachusetts Institute of Technology10 .

The People’s Bank of China (PBoC) is leading the pack with its ready-to-be-launched Digital Currency Electronic Payment (DCEP). China’s size, both in terms of GDP and its financial markets, contrasts with the renminbi’s importance as a reserve currency. At the end of 2020, a mere 2.3% of allocated reserves was denominated in renminbi. This state of affairs likely does not please Beijing, eager to consolidate China as a superpower on all fronts, including trade, military, technology and finance. A digital currency might be the perfect instrument to accelerate the rebalancing of global reserve currencies.

Geopolitical implications of CBDCs: Digital sovereignty

From a historical perspective, the issuance of currency in circulation has been associated with the concept of “sovereignty”. As sovereignty is defined as “supreme authority within a territory”, the state has always been identified with signs such as the flag and the currency issued by the government ruling over a certain territory. When issuing the currency in circulation became the monopoly of the central bank, the institution itself became another typical manifestation of sovereignty (the supreme monetary authority) within a certain territory. As a result, the issuance of CBDCs by a country’s central bank is a way of reasserting the county’s sovereignty over the monetary domain of its cyberspace.

In a narrow sense, digital sovereignty has been defined as the ownership by users of personal data collected by websites with or without their consent. But this risks being too narrow a definition, even if the ownership of data does play a crucial role in the implementation of digital sovereignty. To make it broader, let’s resort to the traditional definition of sovereignty as ‘supreme authority within a territory’, typically defended by an army.

To understand this, it is crucial to define the concepts of ‘authority’, ‘territory’ and ‘army’. In cyberspace, the concept of a territory within a confined border is hard to grasp, although one can reduce it to the location where the data of a country’s citizens is stored. Cloud technologies add a layer of complexity, but while data held in the cloud can be retrieved from anywhere in the world, they are stored in servers located in a specific country.

So who owns this data? The citizens of the country that originated the data? The country where their data is stored? Or the country of origin of the multinational providing the service? In an era in which data is as valuable as oil was in the last century, this could become the cause of geopolitical frictions or even conflict. For example, imagine the data of French citizens stored by Google in Iceland. Can the French government access the data of its own citizens if it is physically stored abroad, and ‘owned’ by a third country, private-sector entity?

If this is the case, we can easily see how there will be pressure in the future from governments to ensure their citizens’ data is physically stored in their country, even when using cloud technology. In Europe, the borders of the European Union are likely to be seen as a national border. The army of the future will be the cyber divisions of traditional armies. Private-sector companies will play a crucial role, just as private contractors do today in traditional conflicts.

From digital sovereignty to geopolitical conflicts in cyberspace

In the last few years, acts of cyber warfare have become increasingly frequent, and recently most hostile attacks by unidentified subjects on sovereign institutions have happened in cyberspace. For example, the Stuxnet attack believed to be responsible for damage to Iran’s nuclear programme in 2010-15, NotPetya, a malware that attacked the Ukraine and impacted international corporates including Maersk in 2016-17, and a large-scale cyberattack and data breach on US federal institutions in 2020.

Without dwelling excessively on the matter of cyber warfare, it is very unlikely that CBDCs will be spared from such cyberattacks. Once the balance sheet of the central bank becomes de facto available for the general public (although potentially only through the wholesale market initially), there is going to be huge temptation for certain parties to try and carry out an attack on its digital currency. The potential damage of a data breach in a CBDC context could be huge, if we consider the information content of new CBDCs.

A cyberattack on CBDCs could represent a violation of digital and traditional sovereignty akin to a declaration of war, in the new digital era. The question is whether countries will adapt their diplomatic conduct fast enough to encompass these potential developments.

Potential use of CBDCs to obtain geo-strategic advancements

Two countries have made the largest progress in the development of CBDCs: China and Sweden. While Sweden does not seem ready to fully roll out its digital currency for four to five years, China’s DCEP system was conceived six years ago and is now in its experimentation phase, with local tests being conducted in Shenzhen, Suzhou, Xiongan and Chengdu. These test programmes have ranged from usage in government services to bill payments and transportation – and several international companies are taking part in these pilot programmes, including US companies such as Starbucks, Subway and McDonalds.

More recently China has started to address the issue of cross-border payments using its CBDC technology by joining the BIS Innovation Hub and Hong Kong Monetary Authority Bridge initiative and their proof-of-concept prototype for wholesale cross-border payments. These tests of settlement will enable banks in four initial countries and regions – China, Hong Kong, Thailand and the United Arab Emirates – to accept payment in any of these four currencies. Participating central banks will be allowed to hold each other’s CBDCs.

China clearly intends to use its digital currency for domestic and international purposes. Domestically, it appears to want to finalise the process that will lead the country to become a fully cashless economy. Given the information content of the new digital currency, one can imagine that – for an autocratic regime such as in China – being able to record any transaction taking place in the economy could be a goal in itself. The possibility of bringing interest rates into deeply negative territory if needed to stimulate demand is an additional benefit, even if the adoption of a digital currency is expected to generate multiplier effects. For example, China bankers estimate that a RMB10m digital currency test could generate a RMB50m increase in sales11 .

Regarding its likely international purposes, China had already begun a process for the internationalisation of its currency way before the CBDC project was conceived. The Chinese financial market is evolving rapidly. In particular, its inclusion in major bond indices has recently raised the profile of the Chinese bond market, which in terms of size is already competing with the largest and most liquid bond markets in the world (Exhibit 4).

- Q8WTdXLDqSAoMjAxOSksIFVwZGF0ZSBmcm9tIHRoZSBDaGFpciBvZiB0aGUgRzcgV29ya2luZyBHcm91cCBvbiBTdGFibGVjb2lucywgc3BlZWNoLCBCSVM=

- QXVlciBldCBhbC4gKDIwMjApLCBSaXNlIG9mIHRoZSBDZW50cmFsIEJhbmsgRGlnaXRhbCBDdXJyZW5jaWVzOiBEcml2ZXJzLCBBcHByb2FjaGVzIGFuZCBUZWNobm9sb2dpZXMsIEJJUyBRdWFydGVybHkgUmV2aWV3LCBBdWd1c3Q=

- RUNCICgyMDIwKSwgUmVwb3J0IG9uIGEgRGlnaXRhbCBFdXJv

- RmVkZXJhbCBSZXNlcnZlIEJhbmsgb2YgQm9zdG9uICgyMDIwKSwgVGhlIEZlZGVyYWwgUmVzZXJ2ZSBCYW5rIG9mIEJvc3RvbiBBbm5vdW5jZXMgQ29sbGFib3JhdGlvbiB3aXRoIE1JVCB0byBSZXNlYXJjaCBEaWdpdGFsIEN1cnJlbmN5

- Q2hpbmEgZ2l2ZXMgJDEuNG0gdG8gbG9jYWxzIHRvIHRlc3QtZHJpdmUgZGlnaXRhbCBjdXJyZW5jeSB8IFRlY2hub2xvZ3kgJmFtcDsgQUkgfCBGaW50ZWNoIE1hZ2F6aW5l

It is no surprise that the supremacy of the US dollar in the international monetary and financial system is a manifestation of the US’s dominant geo-strategic position. At the time of the Bretton Woods conference in 1944, when the post-World War II international financial system was conceived, the US refused to accept the creation of an international “synthetic” currency (such as the bancor proposed by economists John Maynard Keynes and Ernst Schumacher), contributing to what French President Valéry Giscard d’Estaing years later called the dollar’s “exorbitant privilege”. Given these premises, then the dominance of the US dollar in international transactions appears to be a bastion of US supremacy.

While a number of attempts have been made to settle the payments of commodities such as oil in currencies other than the US dollar, China’s attempt to establish the renminbi as an international currency is much more wide-ranging. China appears to have learnt from the US that the imposition of a currency cannot happen without developments in the real economy. In the case of the US, the military expenses of World War II, the Marshall plan, the flow of Foreign Direct Investment into Europe and Asia-Pacific after the war, and becoming a debtor country with a negative current account balance favoured the distribution of the dollar around the world, helping make it the de facto international reserve currency.

In the case of China, the establishment of the Belt and Road Initiative (BRI), the Asian Infrastructure Investment Bank (AIIB) and the recent signing of the Regional Comprehensive Economic Partnership (RCEP) all help to project the country’s economic strength outside the domestic perimeter. What’s more, the plethora of bilateral agreements with several countries, with China helping finance their infrastructure plans (in exchange for a claim on their domestic assets), has made China a preferred creditor, which appears to rule out the possibility of these countries accessing the Paris Club debt restructuring rules12 . Even the recent increased political grip on Hong Kong can perhaps partly be explained by China’s will to establish a stronger control on its major international financial centre.

At the same time, establishing an international currency requires a degree of openness and liberalisation that the regime does not seem ready to accept just yet. The opening of the country’s capital account remains partial at best and the transfer of money abroad remains tightly controlled, if not forbidden in most cases. This could make the case for the internationalisation of the renminbi harder to achieve.

The introduction of China’s digital currency will likely represent an acceleration of existing trends. It is relatively straightforward to imagine that China will “incentivise” the adoption of its own digital currency in all countries within the BRI and AIIB which will not develop their own CBDC. It will likely offer its platform to the RCEP countries, even to those that will begin developing their own digital currency.

In fact, like in geopolitics and in every strategic game, China will likely aim to exploit the first mover’s advantage. For some central banks time itself appears to be an existential asset in the CBDC race. In fact, modelling the introduction of a CBDC in an international interest parity environment might explain the sense of urgency that we see from Beijing – as one report suggests, “That a CBDC increases asymmetries in the international monetary system by reducing monetary policy autonomy in foreign economies, but not domestically, suggests in addition that introducing a CBDC sooner, rather than later, could give rise to a significant first-mover advantage.”13

Will China win the CBDC race?

So the question is this: If China is making such huge strides in the battle for CBDC supremacy, where is the US in all this? Of the major central banks, the Fed seems the one most behind in the development of its digital currency, with even the ECB having recently launched its project for the digital euro. What can explain this apparent sluggishness?

First, the US is generally behind China on a number of cyber fronts, including the development of its own 5G technology in terms of quality and price. Second, it is possible that the US is resting on its laurels, well aware of the existing privilege of the US dollar in the international financial system. Third, the US can always use its regulatory power to impose its own platforms, also thanks to the increased extra-territoriality of its regulations (or sanctions). Fourth, given the amount of resources available, the US could launch a project that eventually catches up with its strategic rivals, as it did with the race to the moon against the Soviet Union.

In the multi-polar world of CBDCs, we expect there will be an effort by the major central banks – the Fed, Bank of Japan, ECB, Bank of England and the PBoC – to gain a strategic advantage over the others, perhaps in terms of adoption of their own platforms by countries in their sphere of influence. In particular, we expect developed markets’ central banks to push back against a perceived too-rapid advancement by China. In fact, in the space of just over 12 years, with the two systemic crises of 2008-09 and 2020-21, China has made a giant leap forward in the ranking of geo-strategic influence, thanks to its ability to withstand these crises better and recover faster than its peers. For example, China is now openly campaigning for the adoption of its own model – a mix of state capitalism, freedom of enterprise and political authoritarianism – by those countries, especially in South-East Asia, that have experimented with democracy, with in our view ambiguous results14 . In this respect, we anticipate that CBDCs will be another battleground of the wider geo-strategic competition that is ongoing among the world’s most powerful countries.

- SG93IENoaW5hIHN0cnVjdHVyZXMgbG9hbnMgdG8gYmVjb21lIEFmcmljYeKAmXMg4oCccHJlZmVycmVk4oCdIGxlbmRlciDigJQgUXVhcnR6IEFmcmljYSAocXouY29tKQ==

- RmVycmFyaSBldCBhbC4gKDIwMjApLCBDZW50cmFsIEJhbmsgRGlnaXRhbCBDdXJyZW5jeSBpbiBhbiBPcGVuIEVjb25vbXksIEVDQiBXUCBuLiAyNDg4

- RGVtb2NyYWN5IEVyb2RpbmcgRmFzdCBpbiBTb3V0aCBFYXN0IEFzaWEsIE1pcmtvIEdpb3JkYW5pLCBSb3NhICZhbXA7IFJvdWJpbmkgQXNzb2NpYXRlcywgQXByaWwgMjAyMS4=

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.