China - Back to normal

- 02 December 2020 (5 min read)

Key points

- Normalising virus conditions, official policies and the natural economy will shape the 2021-2022 outlook

- After effectively containing the virus, any lingering impact of COVID-19 will likely come from offshore

- Reviving natural growth will take over from policy easing to drive the economy further to normality

Rollercoaster ride coming to an end

2020 will go down in history as one of the most challenging years for the global economy since the Second World War. A major public health crisis, triggered by a deadly infectious virus, quickly turned into economic disaster as governments around the world took drastic measures to restrict social mobility and close large portions of economies. At the initial epicentre of the pandemic, China implemented the strictest lockdown of all and saw its economy suffer from a sudden stop. Fortunately, the sacrifice was not in vain. The draconian response proved effective in containing the virus and the pandemic quickly eased. A swift restart of the economy, propelled by significant policy easing, has led to a powerful rebound in economic activities, which is set to make China the only major economy to record positive full-year growth in 2020.

Looking ahead, the 2021 macro outlook will likely feature a further normalisation of the economy, the pandemic and official policies. Some of these normalisations – a firmer control of the virus and restoring organic growth engines – will add to our growth forecast, while normalising policies that lead to reduced stimulus will subtract from it. We will examine each in turn.

COVID can still hurt via trade

As the dominant economic driver of 2020, the coronavirus pandemic has not yet been contained globally. Europe is currently in the midst of a second wave of the pandemic, while the US is confronting a virus resurgence without ever exiting the first wave. China has fared much better in keeping the pandemic under control. While there have been some small “aftershocks” since the initial outbreak, the comprehensive official and public responses – consisting of rapid detention, efficient trace and tracking, widespread testing, strict quarantine, and sometimes mandatory mask-wearing and social distancing – have proven effective in keeping infection numbers significantly below those in the US and Europe. In addition, China is leading the race in developing COVID-19 vaccines. It has three treatments in phase three clinical trials, with the general expectation that at least one will be made available by the end of this year, before a mass rollout in 2021. A safe and effective vaccine will help to further boost public confidence against the virus and accelerate social and economic normalisation.

Given China’s advanced position in fighting the pandemic, we think that any further impact of COVID-19 will likely come more from offshore than within the country. As many of its trading partners are still mired in the pandemic and having to re-engage in lockdowns, China could face reduced demand for its regular exports in the near-term. However, demand for medical-related products will likely remain strong, as will shipments of electronic goods due to a large number of people continuing to work from home. Surging sales of these products, which make up 31% of total exports in 2019, have helped to save China from a severe export contraction.

However, if instead the virus outlook improves following the introduction of a vaccine, normal exports look set to be buoyed by recovering global demand, albeit at the expense of lower sales of pandemic-related goods. China’s well-diversified production base has therefore created a “hedge” for its exports against various paths of the pandemic.

Besides the virus, we expect the US-China trade tensions to de-escalate under a Biden administration, with no more tariff increases next year. However, the bar for rolling back existing tariffs is also high and will likely require China to make concessions in other areas, such as technology, where competition for leadership will remain intense.

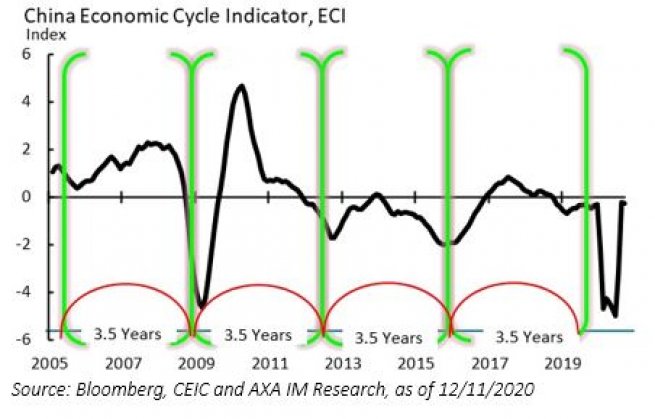

Exhibit 1: Economy regains lost ground

Policy normalisation to shape growth outlook

While the pandemic was responsible for the initial contraction in the economy, the subsequent rebound would not been possible without Beijing’s forceful interventions. Powerful monetary and fiscal stimuli were deployed to keep businesses afloat and employees on payroll during the height of the COVID-19 crisis. Once the pandemic was brought under control, policy easing also played a vital role in facilitating factory reopening and work resumption. Despite being less expansionary than that of many others, China’s stimulus seems to have worked better because its economic rescue came after an effective containment of the virus.

As economic order is gradually restored, Beijing has started to exit its ultra-accommodative policies. The People’s Bank of China (PBoC) has turned more prudent with liquidity injections lately and refrained from using high-profile policy tools, such as reserve requirement ratio and interest rate cuts. This, coupled with better economic data, has led to a rise in onshore bond yields back to their pre-COVID levels. With the price of money back to neutral, the quantity of money – credit and money supply – is expected to follow suit. This should lead to a gradual convergence in credit and nominal GDP growth in 2021, and a stabilisation in the aggregate debt ratio as a result. While the PBoC appears in no hurry to tighten policy due to muted inflation, targeted risk controls for some sectors, such as property, could be stepped up against rising financial imbalances.

Fiscal policy is also heading back to normality. Beijing will likely start by removing some of the emergency measures put in place during the pandemic, such as lowering the fiscal deficit back to around 3% of GDP and eliminating central government special bond issuance. The withdrawal of stimulus will likely be more gradual and data-dependent than monetary policy, to ensure that some supports remain in place to buffer the economy against lingering headwinds.

We also note that 2021 will be the first year of China’s 14th Five-Year Plan, where a zealous official response to some initiatives – such as new urbanisation, technology upgrades and supply-chain enhancement – could raise fiscal spending, offsetting some of the impact from exiting cyclical stimulus. Overall, we expect the normalisation of monetary and fiscal policies to lend less support to the economy in 2021.

Natural growth to take over

The anticipated withdrawal of policy accommodation will be supported by a restoration of organic economic growth. The strong rebound in GDP growth since Q1 2020 was an indication that the economy has started to heal after the devastating COVID-19 shock. Many third-party indicators, such as measures of mobility, traffic congestion, restaurant orders and e-commerce sales, have largely returned to pre-pandemic levels. Our proprietary economic cycle indicator has also rebounded strongly from the bottom and suggests the economy is now within striking distance of trend growth (Exhibit 1).

Importantly, the most recent leg of this recovery has occurred despite reduced policy easing by the PBoC and slower growth in infrastructure investment. These are signs that natural, rather than policy-driven, growth has started to take over as the dominant force behind the recovery.

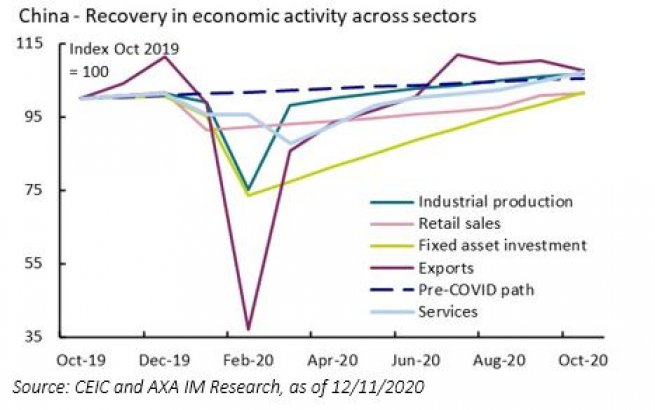

Despite the impressive headline performance, it is important to note that China’s recovery has been uneven across the different sectors. Exhibit 2 shows that while exports and industrial outputs have been quick to get back on their feet, private consumption has lagged behind due to a sluggish labour market and limited official support to shore up household purchasing power. Encouragingly, both job market conditions and consumer spending have improved in recent months. A further normalisation in these activities is expected to create a more balanced macro base from which Beijing can neutralise policies over time.

Exhibit 2: Recovery is strong but uneven

Putting all the moving parts together, we expect China’s annual growth to accelerate meaningfully to 8% in 2021 from 2.3% this year. However, it is worth noting that nearly half of this increase will be due to base effects. In level terms, GDP is projected to be moderately below the pre-COVID trend at the end of 2021. This gap is forecast to close in 2022 when growth reverts back to its trend rate of 5.5% without the base effect distortion.

Risks are substantial but balanced

Overall, our forecast projects an economy that is on path to normality, but not quite getting there until 2022. All three macro forces – the virus, policy operation, and the natural economy – could deviate from our expectations and cause upside or downside surprises to the forecast. Given our base case has already taken into consideration some factors that could slow the economic normalisation process – due to reduced policy support, an uneven domestic recovery and sub-trend growth in China’s trading partners – the risk profile around our forecast is therefore broadly balanced. However, the range of all possible economic outcomes remains wider than usual, reflecting the still-elevated macro uncertainties.

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.