Why biotech’s history of innovation offers exciting opportunities for investors

- 23 February 2022 (7 min read)

The innovation and growth witnessed in the biotech sector over the past two decades have been extraordinary. Together they have created a spate of exciting potential investment opportunities – and we expect the industry’s strong growth prospects to continue into 2022 and beyond.

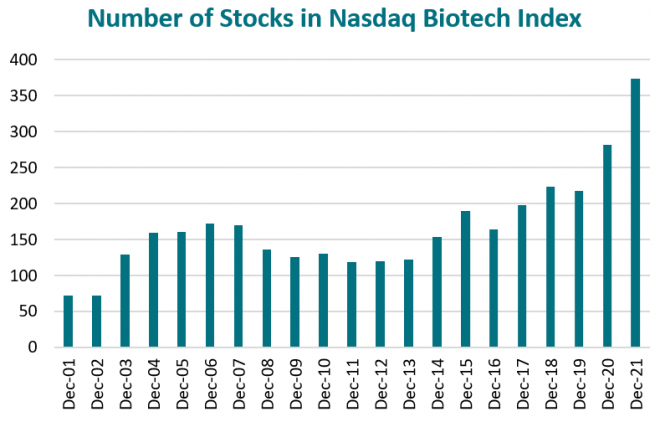

Since 2000, the sector has evolved considerably, from just a handful of companies into a much broader universe spanning well-known names which have had significant commercial successes, to smaller firms engaged in cutting-edge research.

Two decades of innovation and development

The COVID-19 pandemic placed the biotech sector centre stage. Scientists created multiple COVID-19 vaccines within a year – something that was almost unimaginable before – and the collaboration and speed showcased the sector as its best. Companies like Pfizer and AstraZeneca were already well-known outside the investment world, but others like Moderna and BioNTech have become household names thanks to their vaccines. Gilead Sciences also garnered many column inches by being the first to show positive clinical data for its COVID-19 treatment, Veklury (remdesivir).

These companies were already at the forefront of innovation in their fields. For example, Gilead has been a leader in the development of medication to treat HIV for more than a decade. While there is still no cure for HIV, there are now various treatments that enable many people with the virus to live long and healthy lives. And treatment of Hepatitis C – termed a ‘silent killer’ as it causes progressive liver damage – has been revolutionised over the past 10 years with drugs that can cure an infected patient in a matter of weeks.

There have also been huge strides in treating cancer – oncology is probably the most successful area in terms of understanding how a disease is caused by certain genetic mutations and being able to confront those mutations through targeted therapies. For instance, the five-year survival rate for chronic myeloid leukaemia in the US has more than doubled from 31% for patients diagnosed during 1990-1992 to 70% for those diagnosed between 2009-2015, in part due to the discovery of those targeted therapies.1

In addition, during the 21 years since our biotech strategy was launched, we have seen the completion of the Human Genome Project in 2003 to determine the DNA sequence of the entire human genome, underpinning the recent developments of gene therapy. We have witnessed gene editing medicines and better diagnostics including the likely near-term introduction of liquid biopsy for cancer, where biomarkers in the blood can help diagnose the malignancy. We have also witnessed the launch of immune oncology – using the body’s own immune system to aim to prevent and treat cancer – and its journey to become one of the world’s leading therapeutic drug classes.

A broader biotech universe

The scale of the biotech universe has increased markedly over the past decade. As well as money flowing in from investors in the public markets, the sector is also being boosted by private finance, investments from universities and other institutions and government support for start-ups.

This is an exciting time for biotech investors – in the past five years we have seen several small companies launch their first product and start to become profitable, while also developing their drug pipelines.

- QW1lcmljYW4gQ2FuY2VyIFNvY2lldHk=

Relationship with regulators

How biotech firms manage their interaction with regulators around the world is a crucial aspect of drug development and can significantly influence investor sentiment towards the sector.

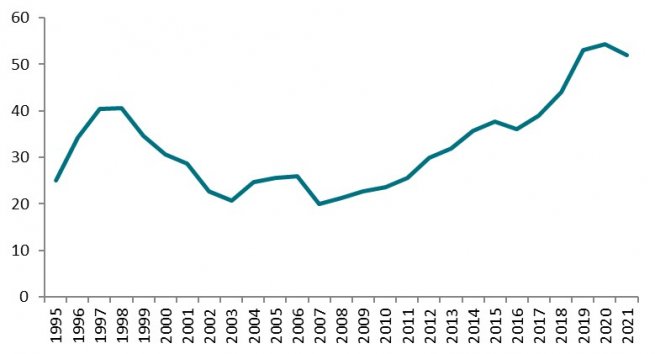

In the past, relationships between pharmaceutical firms and regulators – in particular the US Food and Drug Administration (FDA) - have been mixed, but we believe that over recent years there has been a good working relationship between them. And this correlates with the increasing number of new drugs that have been approved in that period.

What’s more, we believe this trend in approvals is sustainable when you take into account the strong funding in early-stage research, the number of companies that have been formed, the advances which have been made in genetic sequencing, artificial intelligence and more.

Fundamentals remain strong

2020 was a standout year for biotech, due to the positive news flow around COVID-19 vaccines and treatments, with the sector gaining 26.4% over the year. However, in 2021 overall returns for the year were flat despite some gains during the summer.2

It appears a lot of investors decided to move out of stocks which had performed very well, and into shares that were benefiting from the re-opening of the global economy post-lockdown. Simply put, momentum has shifted away from the biotech sector – but the fundamentals have not changed. Cash flows and pipelines remain strong, and there has been some interesting mergers and acquisitions in the sector in recent months – Pfizer announced it would buy Arena Pharmaceuticals, which will expand its pipeline of treatments for immune-inflammatory diseases and Belgian group UCB is in the process of acquiring US firm Zogenix to enhance its epilepsy portfolio.3

Novartis sold its stake in Roche, and GlaxoSmithKline and Pfizer are expected to spin off their consumer healthcare joint venture later this year, giving them further financial resources to potentially conduct future deals. And companies are perhaps operating smarter – making sure they understand the biology that drives a disease before they target it and ensuring it is a condition which needs new therapies rather than creating an alternative to what is already out there.

The next stage

The macroeconomic environment is also important, perhaps more so than ever. A large proportion of the biotech sector is valued on a discounted cash flow basis (as promising but unproven future pipelines make valuations more complex), so rising inflation could weigh on performance in the near term and increase volatility in biotech share prices. Interest rate hikes, which we are starting to see from major central banks, also tend reduce the value of growth stocks.

Tensions between the US and China are likely to remain heightened, and Chinese companies that trade on US stock exchanges through American Depositary Receipts could see their share prices impacted by delisting risks. However, fuelled by government support, a regulatory overhaul, shifting demographics, growing demand for innovative therapies and booming capital markets - the emergence of China in biotech can’t be ignored.

We expect to see more collaboration between Chinese biotech firms and Western pharmaceutical companies, while they continue to build in-house research and development as well as manufacturing capabilities globally. The US FDA’s decisions this year on several applications for drug approvals from Chinese biotechs will likely set the tone for those with global ambitions and steer the direction of their future clinical development.

The US remains the largest market for healthcare and therefore the political environment can exert significant influence on sentiment towards the sector. We will be closely watching the midterm elections later this year – if Republicans gain control of the Senate, this would likely reduce the risk of significant legislative changes, which we believe would be seen as a positive for the sector. However, if the Democrats have a clear majority in Congress, President Joe Biden would have a greater ability to push through changes such as pharmaceutical pricing reforms.

Future drivers

Overall, we expect significant investment to continue going into innovative biotech firms. This year, phase three trial data are due for Alzheimer’s drugs from Roche and Biogen/Eisai, which are expected to be a major driver of sentiment on the sector.4 We are also expecting to see more developments in targeted neuroscience aside from Alzheimer’s – for example Parkinson’s disease, epilepsy and even depression. Gene editing and gene therapy are exciting areas to watch, while further advances in oncology are anticipated, including key lung cancer trial data from Roche.5

Increased awareness and understanding of rare diseases may drive the need for better paediatric care, including early screening for genetic disorders, shortening the journey to correct diagnosis and treating children in the most optimal window of opportunity. At the other end of the spectrum, ageing populations are a key long-term driver for the biotech sector; as we are living longer, we require more healthcare, whether that is treatment for chronic lifestyle conditions or age-related illnesses.

COVID-19 has of course changed the biotech landscape, not least the rapid development and approval of a vaccine. There has been increased focus on healthcare access and inequality, enhanced stakeholder cooperation and greater efficiency, and many of the virtual models for doing business look likely to stay. We take a long-term perspective in relation to the continued presence of COVID-19, which has created a need for healthcare systems to adapt and have taken the opportunity to increase exposure to companies which we believe have the best long-term prospects.

Thanks to a supportive regulatory and demographic environment, as well as research and development investment alongside commercial opportunities, we believe the biotech sector is well-positioned for growth in 2022 and beyond.

- TmFzZGFxIEJpb3RlY2hub2xvZ3kgSW5kZXgsIGluIFVTIGRvbGxhciB0ZXJtcy4=

- Tm92YXJ0aXMgdG8gc2VsbCBpdHMgUm9jaGUgc3Rha2UgaW4gYSBiaWxhdGVyYWwgdHJhbnNhY3Rpb24gdG8gUm9jaGUgfCBOb3ZhcnRpcyAvIEdsYXhvU21pdGhLbGluZSBUbyBTcGluLU9mZiBDb25zdW1lciBIZWFsdGhjYXJlIEJ1c2luZXNzIEJ5IE1pZC0yMDIyIChmb3JiZXMuY29tKSAvIFBmaXplciB0byBBY3F1aXJlIEFyZW5hIFBoYXJtYWNldXRpY2FscyB8IFBmaXplcg==

- SW52ZXN0aWdhdGlvbmFsIEFsemhlaW1lcuKAmXMgRGlzZWFzZSBUaGVyYXB5IExlY2FuZW1hYiBHcmFudGVkIEZEQSBGYXN0IFRyYWNrIERlc2lnbmF0aW9uIHwgQmlvZ2Vu

- Um9jaGUgLSBOZXcgZGF0YSBmcm9tIHRoZSBwaGFzZSBJSSBDSVRZU0NBUEUgdHJpYWwgc2hvdyBlbmNvdXJhZ2luZyByZXN1bHRzIHdpdGggUm9jaGXigJlzIG5vdmVsIGFudGktVElHSVQgdGlyYWdvbHVtYWIgcGx1cyBUZWNlbnRyaXEg

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.