US High Yield Market 2022 outlook

- 17 January 2022 (7 min read)

2022 Outlook Summary

We are anticipating the US High Yield market to return 4-6% in 2022, similar to our previous year’s projection and 2021’s actual return of 5.36%. Our positive outlook is driven by similar themes from 2021, including above average economic growth, continued ultra-low default rates, strong credit metrics, and supportive market technicals. Sources of volatility will continue to center around inflation, Fed messaging, and the impact of new Covid developments. As always, the return for any calendar year will be path dependent, and the timing of when periods of higher volatility occur will impact 2022’s return. Particularly for this year, with the potential for a large percentage of the universe to be upgraded to Investment Grade, the timing of any rate or spread volatility relative to the composition of the universe at that time will impact total return for 2022. Below, we discuss some of the major themes that will impact the US HY market’s expected return.

Valuation limits significant upside to the market’s return in 2022.

After November 2021’s market sell-off drove yields to a 12-month high of 4.85%, the subsequent market rally in December took away some of the potential return for 2022. The US High Yield market begins the year with a YTW of 4.32%, in-line with 2021’s starting YTW of 4.24% and within the 3.78%-4.56% YTW range that occurred during the first 10 months of 2021. However, the US HY market OAS is at 310 to start the year, meaningfully lower than 2021’s starting OAS of 386 and close to 10-year lows.

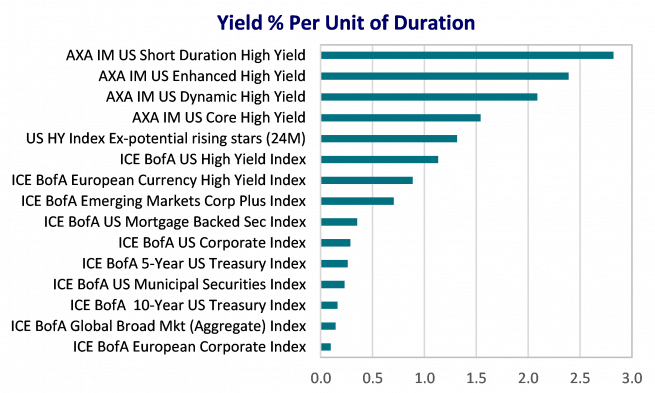

While valuation remains underwhelming from a historical perspective, relative valuation remains attractive when compared to the global fixed income universe. Particularly when focusing on yield per unit of duration, the US HY market still screens as an attractive offering in an overall low, and potentially rising, rate environment.

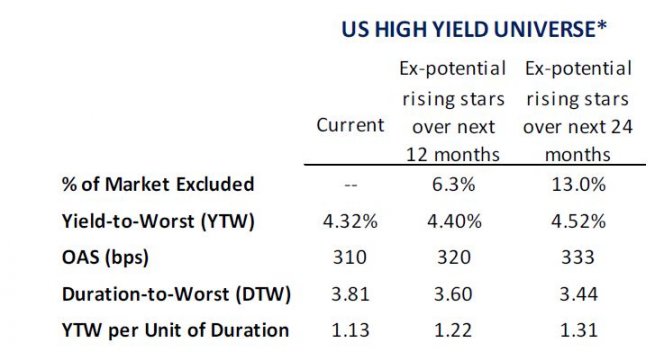

Further, an increasing number of large capital structures within the US High Yield index are expected to be upgraded to Investment Grade. These “Rising Stars” are driving down the yields and spreads of the market while also increasing the duration of the overall market. For US HY market issuers with a weight greater than 0.3% in the index (64 issuers in total), we believe 15 issuers making up 13% in market value of the overall US HY index can potentially be upgraded in the next 24 months. It is difficult to predict when these rating upgrades could happen, and many of these issuers are already owned by Investment Grade investors and trading close to Investment Grade levels. However, as these larger capital structures exit the US HY market, the remaining universe provides a slightly more attractive valuation especially when duration is considered.

While the current impact of 20bps on yield may not be a significant amount by itself, the improvement in the YTW per unit of duration is more meaningful in a rising rate environment. The timing of these upgrades, especially with respect to any potential rate volatility, will have an impact on overall market returns, as the remaining universe will be higher yielding and lower in duration.

The Fed’s management of inflation and interest rate expectations are key sources of potential volatility in 2022.

The Fed’s changing view towards inflation and more hawkish comments may have alarmed some market participants in recent weeks. Ultimately, we believe that the Fed will complete its tapering in the coming months and begin the rate hike cycle, with the additional potential for the Fed to engage in quantitative tightening by selling down its balance sheet. We stop short of projecting any number of rate hikes, as we believe the Fed will leave themselves plenty of room for policy adjustments throughout the year in response to inflation data and the impact from Covid. As for our inflation expectations, we believe there are some concerns for continued rising inflation, but we expect less headline risk from inflation as the “base-effects” begin in the second quarter and year-over-year inflation data becomes less concerning to investors. A risk for 2022 is the potential perception, right or wrong, that the Fed is losing control in managing inflation, which ignites a sell-off in risk assets. We believe this is a key source of potential volatility during 2022.

Covid-19 headlines will continue to be a source of volatility.

We are very hopeful that this is the last year we discuss Covid-19 as a risk to the economic environment, but we will not be surprised if its still a talking point in the months and years to come as investors monitor future variants. We believe most places in the US have little desire to return to economic shutdowns, and instead will prefer to live with the risk, if it remains manageable. For us to be concerned about a sustained economic slowdown and sustained sell-off in risk assets, we think a Covid-19 variant will have to exhibit 3 characteristics: 1) extremely contagious 2) can evade vaccinations and 3) have a high severity of symptoms. The recent Omicron variant certainly covers the first and maybe the second characteristics, but so far the severity has been manageable. We are hopeful this is the dominant variant and we are currently undercounting positive cases. Nevertheless, Covid-19 developments will continue to be a source of volatility in 2022.

Default Rate Expectations and Credit trends remain supportive.

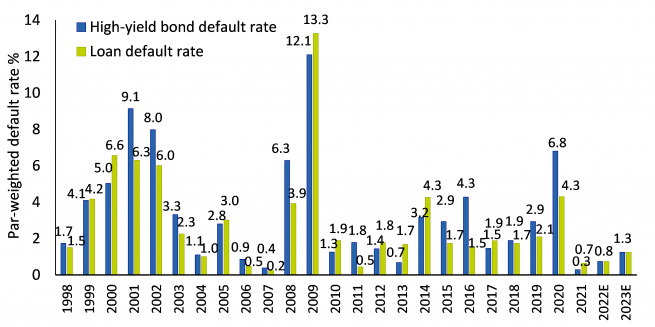

The LTM default rate for the US HY market was just 0.29% at the end of 2021 (J.P. Morgan: Default Monitor January 3, 2022). With above average economic growth and wide-open capital markets providing financing solutions to (the limited number of) stressed credits, it is difficult for us to project a default rate much above 1% in 2022. However, in this low yield and low spread environment, that is arguably priced in already. What will matter in 2022 is avoiding issuers where the potential for default risk emerges, as those securities will face a significant repricing to better compensate investors for that risk.

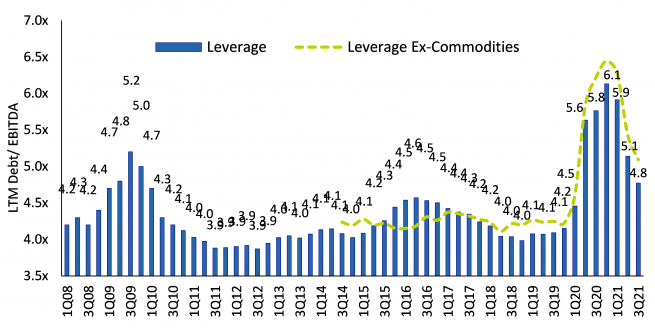

Overall credit metrics also continue to improve as issuers recovered from the pandemic driven economic shut- downs. Leverage has declined sharply from the Q4 2020 highs, and while we expect the rate of improvement to slow in 2022, we still expect continued improvement for the overall market as sectors heavily impacted by Covid move back to 2019 EBITDA levels. One headwind for credit metrics is rising costs, which is impacting some sectors more than others. At this point we don’t believe this will alter default risk expectations, but it is worth carefully monitoring companies with minimal pricing power if inflation continues to be an issue.

A decline in US HY Market supply will provide technical support to the asset class.

As mentioned above, a significant portion of the US HY universe has the potential to be upgraded to Investment Grade and leave the US HY index. While this shifting universe slightly increases the yield and lowers the duration of the asset class, the true impact may be larger as investors rotate out of these newly investment grade rated securities and back into high yield securities, providing an additional technical tailwind. It is also our expectation that new issue supply will be lower in 2022 relative to 2021. This will be driven by a lower amount of refinancing deals and continued strong demand for the US Leverage Loan market, which has the potential to take a greater share of issuers’ financing structures, limiting the supply of unsecured HY bonds available to new issue investors.

Conclusion

Similar to 2021, there are several potential risks on the horizon that could create volatility in the US HY market, including unmentioned risks such as Asian Real Estate contagion, geopolitical risks, and commodity price volatility. However just like at the end of November 2021, we believe that volatility in the US HY market will be short lived and will create buying opportunities due to the positive fundamental and technical considerations we highlighted above. Our coupon-like return expectation of 4-6% for the asset class should ultimately compare favorably to other global fixed income asset classes in 2022.

High Yield Bonds

We offer a range of high yield strategies investing within and across regions, sectors and maturities.

Find out moreDisclaimer

Not for Retail distribution: this document is intended exclusively for Professional, Institutional, Qualified or Wholesale Investors / Clients, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is being provided for informational purposes only. The information has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. This analysis and conclusions are the expression of an opinion, based on available data at a specific date. Due to the subjective aspect of these analyses, the effective evolution of the economic variables and values of the financial markets could be significantly different for the projections, forecast, anticipations and hypothesis which are communicated in this material.

The risk information provided herein is not sufficient to support an investment decision, and is qualified in its entirety by the more complete disclosures, risk factors and other terms available upon request from AXA Investment Managers.

Representative Accounts: Such accounts have been selected based on objective, non-performance based criteria, including, but not limited to the size and the overall duration of the management of the account, the type of investment strategies and the asset selection procedures in place. Therefore, the results portrayed relate only to such accounts and are not indicative of the future performance of such accounts or other accounts, products and/or services described herein. In addition, these results may be similar to the applicable GIPS composite results, but they are not identical and are not being presented as such. Account performance will vary based upon the inception date of the account, restrictions on the account, along with other factors, and may not equal the performance of the representative accounts presented herein. The performance results for representative accounts are gross of all fees and do reflect the reinvestment of dividends or other earnings. The examples of securities provided for each representative account presentation are for illustrative purposes only and are intended to reflect the typical securities, sectors, and/or geographies that could be deployed by the strategy to generate the target returns. These examples do not represent all of the securities purchased, sold or recommended for the client’s accounts, and should not be considered a buy/sell recommendation. An investor’s actual experience may vary.

The Adviser is not a tax or legal advisor. Prospective investors should consult their tax and/or legal advisors before making tax-related and/or legal-related investment decisions.

The ICE BofA ML US High Yield Index is composed of high-yield corporate bonds and other distressed securities. Taxable and tax-exempt US municipal, DRD eligible and defaulted securities are excluded from the Index. Indices are rebalanced monthly by market capitalization. The BofA Merrill Lynch High Yield Index is an unmanaged index consisting of U.S. dollar denominated bonds that are rated BB1/BB+ or lower, but not currently in default. An index is unmanaged and is not available for direct investment.

The AXA IM US High Yield Review is a publication of AXA Investment Managers US Inc. For additional information, please contact us at 100 West Putnam Avenue, Greenwich, CT 06830 USA. Tel: (203) 983-4200.

AXA INVESTMENT MANAGERS PARIS, a company incorporated under the laws of France, having its registered office located at Tour Majunga – La Défense 9 – 6, place de la Pyramide – 92800 Puteaux, registered with the Nanterre Trade and Companies Register under number 353 534 506, a Portfolio Management Company, holder of AMF approval no. GP 92-08, issued on 7 April 1992.

Issued by AXA Investment Managers UK Limited, which is authorized and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 7 Newgate Street, London EC1A 7NX.

© 2022 AXA Investment Managers US Inc. All rights reserved.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.