Gilt trip: Lessons for institutional credit investors from a UK liquidity crisis

- 24 October 2022 (7 min read)

Key points:

- UK government debt (gilts) suffered a sharp repricing following a government mini budget which implied heavy additional borrowing and the prospect of steeper rate increases

- Despite extreme bond market volatility, we were able to help all our UK defined benefit pension fund clients who required rapid access to cash to make the required collateral calls

- We think this experience demonstrates how a thoughtful long-term credit strategy could provide both hedging characteristics for pension scheme liabilities and growth potential

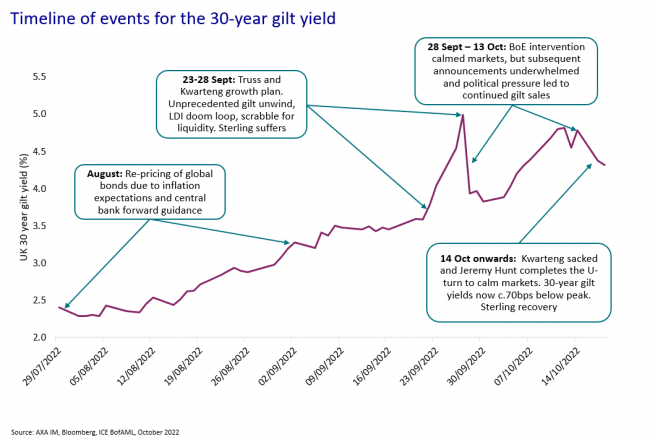

It has been an extraordinary few weeks in UK politics, and a worrying time for some of the country’s largest investors. A ‘mini budget’ intended to encourage growth instead rattled markets. The Bank of England (BoE) rushed to intervene, Chancellor of the Exchequer Kwasi Kwarteng was fired and his replacement reversed most of the announced measures. In any circumstances, this would be a difficult environment for investors. But these events offered a particular challenge for many pension schemes, and we think provide some lessons about the potential advantages of well-structured allocations to corporate credit.

The reaction to the mini-budget was swift, with 30-year-gilt yields rising to peak at over 5% on 27 September, levels not seen since the 2008 financial crisis (source: Bloomberg). Sterling fell to as low as $1.03 from around $1.15 in the days before the now-former Prime Minister Liz Truss took office (Source: Bloomberg).

As markets priced-in deep uncertainty about the future course of the UK economy, there was a dramatic effect on defined benefit pension schemes that were using leveraged liability-driven-investment (LDI) strategies with gilts deployed as collateral for related hedging. In short, as the value of gilts dropped, they started receiving margin calls from their banks and had to assess rapidly how they would meet those cash demands. Sterling’s woes sharpened the stress.

Liquidity test

It has been a tumultuous period, one which has reminded us that liquidity is a cornerstone of investment and one which has seen AXA IM successfully raise all the money our clients have requested and with reasonable transaction costs, in our view, given the market turmoil. Indeed, we think these dramatic weeks have been a useful test of the resilience of long-term credit allocations in a moment of market stress.

Looking at the effect on credit markets, and excluding a spike seen during the COVID-19 pandemic, spreads climbed to highs not seen in 10 years. The UK credit spread to government debt has doubled since the fourth quarter of 2021, from 112 basis points (bp) to 244bp.1 It truly was a technical rerating of the whole market, with even AAA-rated bonds feeling the pressure and spreads widening across all maturities.

In practical terms, our clients’ credit portfolios offered the liquidity required to meet their obligations. Transaction costs were elevated, as might be expected, and were about two and a half times that seen in normal times, based on our observations. That was in part driven by the sharp volatility in the normally placid gilt markets.

Under the bonnet

In the days that followed Kwarteng’s mini budget, our primary goal was to act decisively to meet all client requests in the most efficient way possible – including instances where we provided liquidity within a day of receiving an instruction. We have always aimed to build long-term portfolios that remain responsive to short-term needs for flexibility. It has been encouraging to test that premise.

As we worked to assist our clients, we found that the structurally long-duration and high-quality nature of many of those credit portfolios was actually doing a lot of the hedging for pension funds already. This had given some the room to run less leverage within their LDI strategy and therefore relatively less exposure to this technical liquidity event.

For those that did need to make sales, we focused on the most liquid parts of the portfolio, often sovereign and quasi-sovereign bonds. Another area we focused on was non-sterling allocations. We commonly hold modest amounts of dollar- and euro-denominated credit in sterling portfolios and given the localised nature of this crisis, it clearly made sense to exploit these holdings from a relative value perspective. Overall, we tried to use shorter-dated credit in order to reduce costs and not change the composition of the portfolio too much.

We think this crisis has helped emphasise the potential importance of credit for UK pension schemes, and meanwhile, the swift reversal of significant parts of the package has indeed stabilised conditions. At the moment, credit feels like a good two-way market, especially for schemes. Some are consolidating and reviewing their collateral positioning, perhaps looking to raise funds from credit. But also, credit may appear relatively attractive right now in terms of valuation and spread, conditions which are pushing some clients to opportunistically add credit, sometimes using collateral that was raised and which is no longer needed. Other clients are exiting less liquid asset classes and using those flows to increase credit allocation.

Credit where it’s due

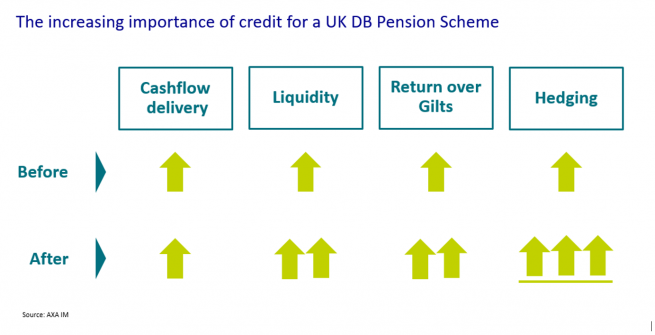

Over the longer term, we continue to see fundamental benefits of credit for pension schemes and expect many of those benefits to be bolstered in the aftermath of this crisis. Cashflow delivery to pay pensions is a given, of course, but the potential liquidity and spread advantages have been underscored by recent events. The same is true, we believe, of that potential hedging capability of well-managed, long-term credit allocations.

- U291cmNlOiBBWEEgSU0sIElDRSBCb2ZBTUwsIEJsb29tYmVyZywgMTcuMTAuMjAyMg==

Importantly, we have now seen confirmation that credit can provide liquidity as needed at times of painful market stress as well as in more normal conditions. As schemes look ahead to their longer-term objectives and potentially a buyout, this experience may be useful.

Meanwhile, the market outlook for long-term sterling credit portfolios has improved significantly, in our view, even though it has been a very rocky road to get there.

Credit fundamentals in general may well have seen a deterioration, but we believe careful, active management should be able to reveal potential upsides in high-quality, selected names. One observation we have made is that credit has moved from what was quite a tight market with more buyers than sellers to a fundamentally wide market within which clients may be well rewarded for taking on extra risk, in our view. Returns, after all, are needed to close deficits and meet payments over the longer term and credit’s prospective return over gilts is clearly attractive at this point.

We have also been engaging with issuers to encourage them to issue credit that meets our clients’ needs in terms of governance and maturities. AXA IM has a long sought to deliver tangible benefits from engagement across asset classes – most obviously around responsible investing and environmental, social and governance (ESG) matters – and we think we have been able to use this experience to help drive the supply of credit available for our clients that can complement holdings in sovereign debt.

As we look ahead, we expect a step change in how pension schemes think about leverage following this sharp reminder of its role in so many crises. At its simplest, we think LDI leverage will have to come down and that schemes will have to look instead at asset classes that can provide an effective hedging alternative. Our experience over the last month has indicated that long-dated credit could potentially form part of that solution.

GLOSSARY

Yield: A measure of return from interest or dividend income expressed as a percentage of an asset's price. In bond markets, the yield would tend to be higher for debt deemed to be a higher risk. The yield moves in the opposite direction to a bond’s price. (Source: AXA IM)

Spread: The amount of extra yield a bond offers investors over and above the current yield on that country’s government debt. Normally expressed in basis points, with one basis point equalling 0.01%. The term can also refer to the difference between the bid and the ask price of a single security. (Source: AXA IM)

Liquidity: This refers to cash flow, or how easily an asset can be converted into cash. Shares which can be bought or sold rapidly on the stock market are considered a liquid asset whereas a commercial property would be considered more illiquid as it is much more cumbersome to sell. (Source: AXA IM)

Liability: Driven Investment (LDI): A technique for managing pension funds that is designed to protect schemes from adverse movements in interest rates and inflation, and to reduce the impact on funding levels when interest rates fall. LDI strategies may use leverage and derivatives as they seek to protect schemes from risks that might prevent them from making required payments to members. (Source: AXA IM, Reuters, Pensions Regulator)

Derivatives: Investments whose value depends on the changes in the price of an underlying asset or security. For example, instead of holding a stock directly, a derivative is a contract to buy or sell a stock at a set price in the future, and investors seek to profit from the difference between the predicted and actual outcome. The use of derivatives can result in greater fluctuations of a fund's value and may cause the fund to lose as much as, or more than, the amount invested if the price moves sharply against them. (Source: AXA IM)

Leverage: The use of debt to increase the potential return of an investment. Investors can use existing assets as collateral for that debt. (Source: AXA IM)

Margin call: A request for additional funds from a financial counterparty where assets held as collateral for a debt fall in value. (Source: AXA IM, Washington Post)

Hedging: A transaction involving derivatives that aims to reduce a particular financial risk. For example, buying assets in another currency to offer mitigation for an unfavourable move in foreign exchange markets. (Source: AXA IM)

Short positions: Betting an asset price will fall. Investors most commonly are ‘long’ – they buy assets they think are undervalued, have potential for growth, or which they hope will deliver consistent returns over time. A ‘short’ position involves selling a borrowed security with the expectation of buying it back at a lower price to make a profit. However, if the security goes up in value, a short position will make a loss. (Source: AXA IM)

Hedge funds: Pooled investment vehicles that can invest in a wide variety of products, including derivatives, foreign exchange, and publicly traded securities. Hedge funds tend to have more flexibility in the strategies they can pursue and may invest in relatively risky or illiquid assets. (Source: AXA IM, CFA Institute, US Securities and Exchange Commission)

Institutional Featured Solutions

We help institutional investors by building innovative and sustainable custom solutions to support ever-evolving financial, regulatory and stakeholder needs.

Find out moreDisclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Past performance is not a guide to current or future results. The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested. Exchange-rate fluctuations may also affect the value of their investment.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.