Ten years of Mid Cap

- 03 March 2021 (3 min read)

This month marks a decade of managing the AXA Framlington UK Mid Cap Fund. While the past decade has been volatile, featuring the Eurozone Crisis, Brexit and COVID-19, mid cap companies (represented by the FTSE 250 excluding Investment Trusts index) have performed strongly. The FTSE 250 ex IT has almost doubled in ten years, with many companies posting returns far in excess of that.

A decade of change

Part of the attraction of the mid cap universe is its continual evolution, with new companies entering the market as a result of the public listing process and leaving as they are promoted to the FTSE 100, demoted to the FTSE Small Cap or taken private/acquired by other listed businesses.

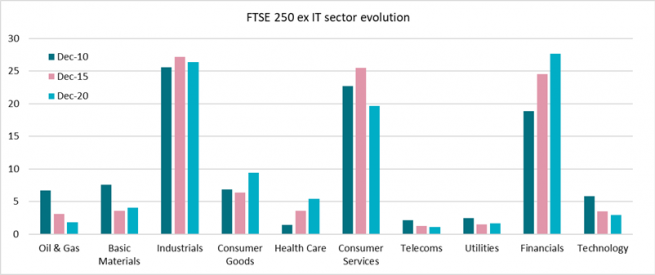

The chart below shows how the market has changed over the past decade, with the declining importance of extractive industries one of the big shifts. The Financials sector has seen the most significant increase in weight, largely due to the increase in real estate investment trusts. Although banks make up a small weight within this index (1.9% at the end of December 2020), there were no banks in 2010, further demonstrating that the mid cap index is continually changing.

Technology representation within the mid cap space has always appeared low (through the above sector split), relative to other regions. Although pure play software & computer services and technology hardware & equipment companies make up a small proportion of the FTSE 250 ex IT index, we would argue that there are many UK business with differentiated, innovative technology within their businesses, with this ‘hidden’ technology driving competitive advantage.

For example, Roke, a business within Chemring Group, has a cyber security services and solutions division which provides effective and efficient information security to the UK government and corporate clients. Technology is clearly a key asset within this space. Roke is able to leverage its technological knowledge base and use its intellectual property to provide solutions to its clients.

Investing in good quality companies over the long term can pay

The following are a few examples of businesses that are, or were, held in AXA Framlington UK Mid Cap fund, which have contributed positively to performance since the fund was launched.1

Ashtead Group is a plant hire company with operations in the US (around 90% of its revenues), UK and Canada. Revenues at the company have roughly doubled since 2016, with profit before tax up by just over 50%.2 Ashtead has benefited from a number of structural and cyclical drivers, such as the shift in their customer base from construction plant ownership to rental. The high service levels that the company offers gives it a clear competitive advantage.

Dunelm is the UK’s largest home furnishing retailer. The business has evolved over time from a pure store-based retailer to one with an online offering too. By understanding the behavioural shifts in its customer base, Dunelm has developed a multi-channel offering, enabling it to benefit from the acceleration in the shift to online due to the pandemic.

Rightmove is the UK's largest online real estate portal and property website and has developed a sophisticated, but simple to use platform which has seen it take market share over the years and become the go-to website/app. The business has continually developed tools to increase its offering to both estate agents and house hunters.

Booker is a leading food and drink wholesale provider in the UK. The business merged with Tesco in 2018 to enhance the enlarged company’s growth prospects by creating the UK’s leading food business with combined expertise in retail, wholesale, supply chain and digital.

Betfair is an online gambling company which operates the world's largest online betting exchange and is another example of a business which has combined with another since listing on the stock market. The company merged with Flutter Entertainment, formally known as Paddy Power, in 2016, strengthening the broader online and offline betting offering.

Ten more years?

Plenty has been written about the attractiveness of the UK market, particularly in recent months. The key point looking back over the past ten years is that the political and market backdrop may not necessarily need to be positive in order to benefit from investing in the long-term growth of UK Mid Cap companies.

The performance of the AXA Framlington UK Mid Cap fund demonstrates that by implementing an investment process which seeks to identify and invest in companies that are capable of growing their economic output and compounding their earnings over time consistently, positive performance can be achieved.

We don’t know what the world will look like in ten years’ time, and whether the fund will have continuously held businesses for 15 or even 20 years. What we can say with a high degree of certainty, however, is that the FTSE 250 ex IT will continue to offer opportunities for active investors, much as it has done since its creation.

Stocks mentioned in this article are for illustrative purposes only and do constitute a recommendation to buy or sell individual shares.

Liquidity Risk: some investments may trade infrequently and in small volumes. As a result the Fund manager may not be able to sell at a preferred time or volume or at a price close to the last quoted valuation. The Fund manager may be forced to sell a number of such investments as a result of a large redemption of units in the Fund. Depending on market conditions, this could lead to a significant drop in the Fund's value and in extreme circumstances lead the Fund to be unable to meet its redemptions. Further explanation of the risks associated with an investment in this Fund can be found in the prospectus.

- RnVuZCBsYXVuY2ggZGF0ZSAwNC8wMy8yMDEx

- QXNodGVhZCBHcm91cCBBbm51YWwgcmVwb3J0ICZhbXA7IGFjY291bnRzIDIwMjA=

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This promotional communication does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee that forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Before making an investment, investors should read the relevant Prospectus and the Key Investor Information Document / scheme documents, which provide full product details including investment charges and risks. The information contained herein is not a substitute for those documents or for professional external advice.

The products or strategies discussed in this document may not be registered nor available in your jurisdiction. Please check the countries of registration with the asset manager, or on the web site https://www.axa-im.com/en/registration-map, where a fund registration map is available. In particular units of the funds may not be offered, sold or delivered to U.S. Persons within the meaning of Regulation S of the U.S. Securities Act of 1933. The tax treatment relating to the holding, acquisition or disposal of shares or units in the fund depends on each investor’s tax status or treatment and may be subject to change. Any potential investor is strongly encouraged to seek advice from its own tax advisors.

Past performance is not a guide to current or future performance, and any performance or return data displayed does not take into account commissions and costs incurred when issuing or redeeming units. The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested. Exchange-rate fluctuations may also affect the value of their investment. Due to this and the initial charge that is usually made, an investment is not usually suitable as a short term holding.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.