Why China’s bond defaults could ultimately boost investor confidence

- 08 February 2021 (5 min read)

Despite heightened levels of distress in China’s US$15trn credit space1 , investors stand to potentially benefit from a new path for the onshore and offshore markets as they more efficiently price credit risk.

At first glance, several high-profile bond defaults in late 2020 are a justified cause for concern. This trend might well continue this year, too. If so, it has the potential to create tension with the country’s post-COVID-19 economic rebound – but the short-term impact might well provide potentially longer lasting benefits.

Given that the affected names are state-linked companies with relatively weak fundamentals, increasing differentiation is emerging in this cluster of issuers. In turn, this reflects the broader strategic vision of the government to enhance the overall quality of the fixed income landscape.

This doesn’t downplay the situation. The default by chipmaker Tsinghua Unigroup, for instance, on $450m of debt, also triggered cross-defaults on another $2bn – equivalent to almost two-thirds of total defaulted debt in China’s offshore bond market in 2019.2 Other state-owned enterprises (SOEs) to default included mining firm Yongcheng Coal and Electricity Holding Group and Huachen Automotive Group Holdings.

While the trio of defaults theoretically raises systemic risk, in practice we think this does not pose an ultimate risk to the onshore financial system.

Before this flurry, corporate defaults had been edging higher for around six years. This has been in line with a growing acceptance of market mechanisms due to Chinese government regulators’ preference for deleveraging and generally reforming funding practices.

The government would potentially rather see deleveraging through voluntary restructuring where losses can be absorbed in an orderly manner broadly across the market.

Notably for investors, a positive implication of the defaults will likely be a more efficient debt market as well as more disciplined and effective investment on the part of issuers. In short, the knock-on effect might improve the accuracy of pricing risk and enhance transparency. This aligns with efforts by the People’s Bank of China (PBoC), the country’s central bank, to strengthen its oversight of the ratings industry.

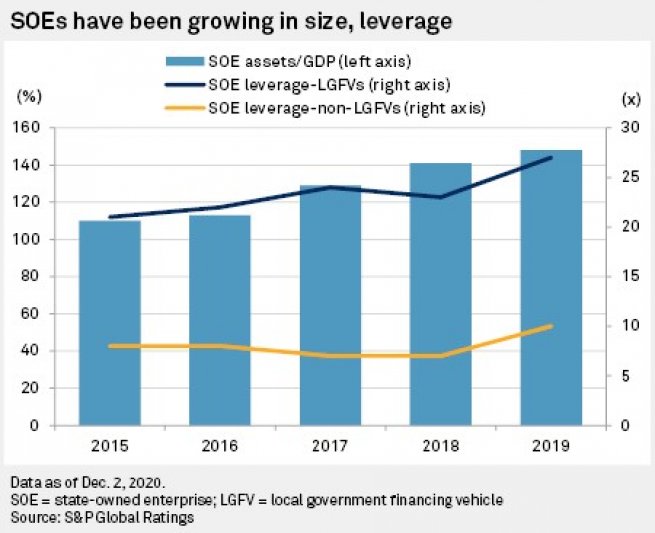

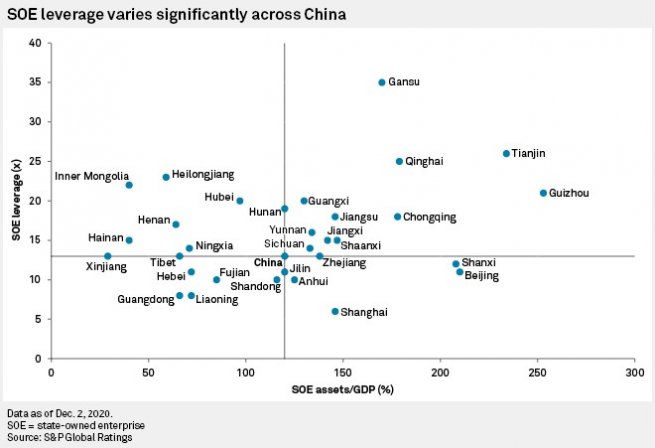

LGFVs in China: Rising leverage, rising issuance and the need for investor discretion

The defaults and subsequent depressed investor sentiment in the short term have also shone a spotlight on bonds issued by local government financing vehicles (LGFVs).

These are an important and growing segment of the both the offshore and onshore Chinese corporate bond markets – and one which cannot be ignored, by investors or government regulators, as a result of high debt levels and relatively low operational transparency.

- aHR0cHM6Ly93d3cuYmxvb21iZXJnLmNvbS9uZXdzL2FydGljbGVzLzIwMjAtMTItMTEvaW52ZXN0b3JzLWFyZS1sZWFybmluZy10by1saXZlLXdpdGgtY2hpbmEtcy1jb3Jwb3JhdGUtZGVmYXVsdHM=

- dHRwczovL3d3dy5ibG9vbWJlcmcuY29tL25ld3MvYXJ0aWNsZXMvMjAyMC0xMi0xMS9pbnZlc3RvcnMtYXJlLWxlYXJuaW5nLXRvLWxpdmUtd2l0aC1jaGluYS1zLWNvcnBvcmF0ZS1kZWZhdWx0cw==

While no LGFV borrower has yet defaulted on a bond, they are not a safe haven. And in keeping with the hunt for quality amid growing investor risk aversion, new issuance is likely to come from LGFVs in more developed regions such as Zhejiang and Jiangsu provinces.

With this in mind, it’s widely expected that the impact of recent defaults on investor appetite for many otherwise high quality, higher visibility LGFVs will only be short-lived given their important public policy roles. In addition, these vehicles benefit from ample liquidity onshore and usually have diverse credit profiles.

In fact, Moody’s predicts LGFV bond issuance in both the onshore and offshore markets will increase in 2021 from last year’s levels. In particular, increasingly attractive international funding costs have the potential to boost offshore issuance this year from a low base in 2020.5

Recent data from Moody’s

| Debt outstanding as of Sept 20, 2020 | Onshore (in RMB trillion) | % of total | Offshore (in USD billion) | % of total |

| LGFV | 10.5 | 41.0% | 77.3 | 13.2% |

| Total corporate | 25.5 | 584.2 | ||

| Sourced & LGFV defined by Wind | Sourced from Bloomberg & Dealogic; LGFV defined by Bloomberg | |||

This is partly due to how post-pandemic themes will likely support LGFVs. A certain bullishness among onshore investors is based on their perception of government efforts during the pandemic, including investing in infrastructure to ensure social and financial stability. Fitch Ratings, for instance, has cited the potential for LGFVs to leverage their experience to help spearhead such an initiative.6

For offshore investors, meanwhile, the refinancing of US dollar-denominated bonds by repeat issuers such as Yiwu State-Owned Capital Operations, have been well received, evidenced by large investor over-subscriptions and narrowing spreads7

. In 2021, roughly $25bn of bonds are due for repayment or refinancing8

. Plus, the need to diversify funding channels might drive more debut LGFV issuers to the offshore market.

More prominent in portfolios

Scepticism among some investors about LGFVs can be tempered by the fact they are state-owned. Further, being controlled by a local or regional government is not necessarily inferior to central government ownership.

As a subset of SOEs, therefore, LGFVs can be evaluated in a similar way in terms of clarity of purpose and strategic importance when determining how much credit enhancement state ownership contributes.

According to S&P Global Ratings, ongoing SOE reform is feeding through to LGFVs. The rating agency believes that over the long term, off-budget risks will be better controlled as LGFV borrowers become more disciplined – for example, improving debt coverage by growing their own revenues.9

China’s Financial Stability and Development Committee has lent weight to this view. In late November 2020, in a meeting to regulate bond market development and maintain stability, the outcome was a stance of zero tolerance towards illegal activities, including fraudulent issuance, fraudulent disclosures, malicious asset transfer and fund embezzlement.10

At the same time, more defaults are inevitable and – in our view, from a big picture perspective – necessary to improve market efficiency. Our previous research, for example, highlighted that single-B issuers globally default at an average annual rate of close to 3%, and 20% cumulatively over a five-year period11

. The cost of funding innovation in an economy will be some level of credit defaults.

The key to ensuring that defaults don’t lead to widespread disruption is transparency around these risks and efficiency in terms of pricing and placement of credit risk. By many indications, China is working towards these goals for the benefit of increasing investor confidence over the long term.

All companies mentioned are for illustrative purposes only and should not be considered as advice or a recommendation for an investment strategy.

- aHR0cHM6Ly93d3cubW9vZHlzLmNvbS9yZXNlYXJjaC9Nb29keXMtUmVjZW50LVNPRS1ib25kLWRlZmF1bHRzLXdpbGwtaW5jcmVhc2UtY3JlZGl0LWRpZmZlcmVudGlhdGlvbi1vZi0tUEJDXzEyNTY3ODQ=

- IGh0dHBzOi8vd3d3LmZpdGNocmF0aW5ncy5jb20vcmVzZWFyY2gvaW50ZXJuYXRpb25hbC1wdWJsaWMtZmluYW5jZS9jaGluYS1uZXctaW5mcmFzdHJ1Y3R1cmUtcHVzaC1vZmZlcnMtbGdmdnMtb3Bwb3J0dW5pdGllcy1jaGFsbGVuZ2VzLTE4LTA4LTIwMjA=

- aHR0cHM6Ly9maW5hbmNlLnlhaG9vLmNvbS9uZXdzL3lpd3Utc3RhdGUtb3duZWQtY2FwaXRhbC1vcGVyYXRpb24tMDczNDEwMTI3Lmh0bWw=

- aHR0cHM6Ly93d3cubW9vZHlzLmNvbS9jcmVkaXRmb3VuZGF0aW9ucy9Mb2NhbC1Hb3Zlcm5tZW50LUZpbmFuY2luZy1WZWhpY2xlcy1MR0ZWLWluLUNoaW5hLTA1RTAwNT9jaWQ9QTUxMkFJUjFQWjkzMDA=

- aHR0cHM6Ly93d3cuc3BnbG9iYWwuY29tL21hcmtldGludGVsbGlnZW5jZS9lbi9uZXdzLWluc2lnaHRzL2xhdGVzdC1uZXdzLWhlYWRsaW5lcy9jaGluYS1zLXJlY2VudC1zdGF0ZS1saW5rZWQtYm9uZC1kZWZhdWx0cy1wb3NlLWxpbWl0ZWQtc3lzdGVtaWMtcmlzay04MjExLWFuYWx5c3RzLTYxNzIwODI1

- aHR0cHM6Ly93d3cuY2FpeGluZ2xvYmFsLmNvbS8yMDIwLTExLTIzL3RvcC1maW5hbmNpYWwtcmVndWxhdG9yLXBsZWRnZXMtemVyby10b2xlcmFuY2UtZm9yLWRlYnQtZG9kZ2Vycy0xMDE2MzE1MzAuaHRtbA==

- U291cmNlOiBBWEEgSU0sIGJhc2VkIG9uIGRhdGEgZnJvbSAxOTkwLTIwMTZIMSBNb29keeKAmXM=

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This promotional communication does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee that forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Before making an investment, investors should read the relevant Prospectus and the Key Investor Information Document / scheme documents, which provide full product details including investment charges and risks. The information contained herein is not a substitute for those documents or for professional external advice.

The products or strategies discussed in this document may not be registered nor available in your jurisdiction. Please check the countries of registration with the asset manager, or on the web site https://www.axa-im.com/en/registration-map, where a fund registration map is available. In particular units of the funds may not be offered, sold or delivered to U.S. Persons within the meaning of Regulation S of the U.S. Securities Act of 1933. The tax treatment relating to the holding, acquisition or disposal of shares or units in the fund depends on each investor’s tax status or treatment and may be subject to change. Any potential investor is strongly encouraged to seek advice from its own tax advisors.

Past performance is not a guide to current or future performance, and any performance or return data displayed does not take into account commissions and costs incurred when issuing or redeeming units. The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested. Exchange-rate fluctuations may also affect the value of their investment. Due to this and the initial charge that is usually made, an investment is not usually suitable as a short term holding.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.