Cheap as gilts

The UK Chancellor’s statement to Parliament on 26 March did little to help the sterling bond market. Yields are higher than in the US and much higher than in the Eurozone. There is little market confidence in the Bank of England (BoE) cutting interest rates much further. The outlook for growth and inflation is poor but there is value in the gilt market. As the trade war shifts up a gear and equity markets potentially come under more pressure some of that value might start to be realised.

Dismal

The UK Office for Budget Responsibility (OBR) revised down its 2025 economic growth forecast to 1.0%. In the report that accompanied Chancellor Rachel Reeves’ Spring Statement, the agency provided a list of concerns for the UK’s economic outlook. Compared to its report of last October, the OBR expects productivity to be lower, inflation to be higher and described the fiscal outlook as having deteriorated. The forecasts are also sensitive to any changes in gilt yields, inflation and international developments. It was not happy reading. And the statement’s details on fiscal policy didn’t provide much to alleviate the gloom. Tariffs, volatile international energy prices, and the need to spend more on defence leave little room for any upside in the outlook.

Low prices, high yields

After briefly rallying on news that the UK’s Debt Management Office may need to sell less long-dated government bonds in the next fiscal year, the gilt market has since resorted to what it does best – underperform. The benchmark 10-year gilt yield knocked on the door of 4.8% this week, and yields on some longer maturity gilts are well above 5%. A gilt maturing in December 2055 has a yield to maturity of 5.35%, 85 basis points (bp) above the current base rate. A similar maturity in the US Treasury market yields 4.73%, just 23bp above the current Fed Funds overnight rate. In Germany, the 30-year Bund yields 66bp above the European Central Bank’s deposit rate – prior to the announcement of Germany’s defence and infrastructure spending plans, the 30-year yield was below the deposit rate. The difference between the 10-year gilt yield and the 10-year Overnight Index Swap (OIS) – a market measure of the future expected level of the overnight interest rate – has risen to 50bp, up 20bp since the election. The UK gilt market yield curve has seen an increase in its embedded risk premium.

Vigilantes

Bond markets punish government borrowers when the fiscal outlook is unclear. France suffered in 2024, and its 30-year yield is still high at 4.2%. Meanwhile yields in Italy and Spain have been declining relative to the German level, which tells us a lot about the relative direction of travel for fiscal policy in Europe. The UK’s issue is that it has a growth and an inflation problem. Yes, February’s consumer price inflation rate came in a little better than expected, at 2.8% compared to expectations of 3.0%, but it is still above target and is set to rise again in the coming months because of budget-related price increases.

How to boost growth

The BoE should cut rates in my opinion. The economy needs some stimulus, and the government might be wise to think about reducing the tax burden rather than following through on National Insurance tax increases. Working towards a more frictionless trading relationship with the European Union would also be welcome. The inflation targeting framework is inadequate when inflation is impacted by policy decisions and the risk is that if households don’t see help elsewhere (lower mortgage costs, for example) then wage growth will remain stubbornly high (even with unemployment likely to go up). But the Bank has been reluctant to endorse further easing. Looking at the OIS market, there is not much expectation that UK rates can fall below 4.0% over the medium term.

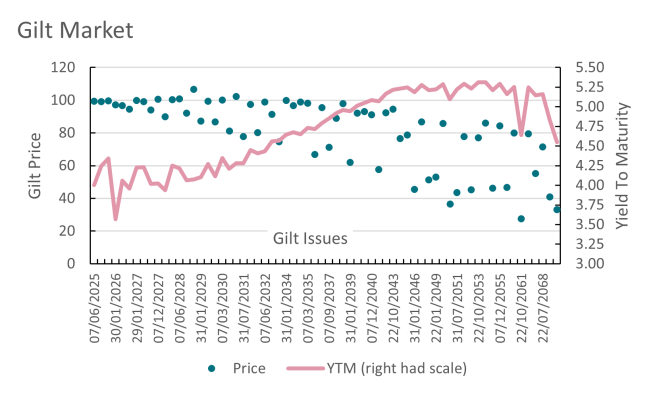

Value in gilts

The term premium looks to have risen in the UK bond market, which gives gilts something of a valuation attraction relative to other major bond markets. The chart below plots the prices and yields-to-maturity of outstanding gilt issues. Some of the prices are very low, especially on low coupon bonds issued during the quantitative easing period. A gilt maturing in October 2061, for example, is priced at just 27 (relative to par of 100). There is upside potential, but the market needs to be more confident about policy on both the monetary and fiscal sides. With Donald Trump’s trade war stepping up, navigating monetary policy is going to be even more difficult. On balance it is hard to see what stimulates growth in the short term (meaning locally and globally), and the downside risks to investor, business and consumer confidence are evident. Bonds should do better in this environment.

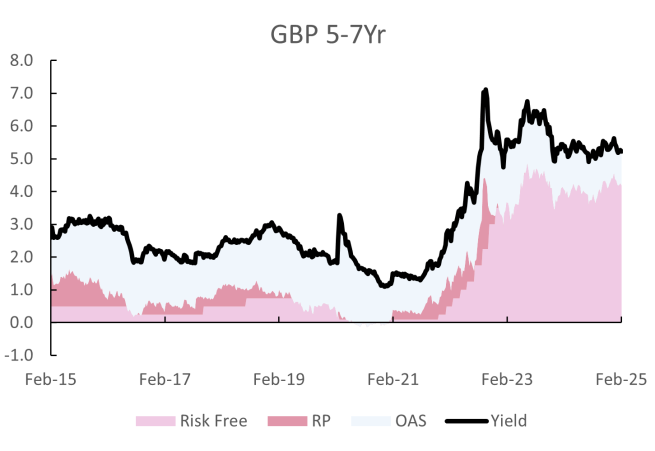

No compensation for duration

Although the UK risk premium has gone up, for most bond markets, yield curves are flat and there is not much compensation for taking duration risk. De-composing credit market curves, it is the underlying risk-free rate, and the credit spread that dominate prospective returns. Across the US dollar, euro and sterling credit markets, there is not much term premium for being in the longer end of the curve than in the shorter end, other than slightly higher credit risk premiums (which is normal, given that there is more uncertainty about an issuer’s credit profile over longer time horizons). Taking data from the ICE Data Services indices on the sterling investment grade market, there is a 50bp yield difference between the one-to-three year and the seven-to-10 year buckets (but a difference of almost five years in terms of duration). The second chart plots the decomposition of the five-to-seven year part of the market in terms of the risk-free rate, the spread between five-year gilt yields and the bank rate (proxy for risk premium), and the credit spread (you can’t see the term premium since 2022 given the flatness of the curve).

Bonds for risk-off

The announcement of 25% tariffs on car imports to the US added to global tensions on trade. The stock market doesn’t like this and the S&P 500’s mini rally was fading as I wrote this note. There is a risk-off feeling to markets and bonds should benefit from that. I like gilts, I like short-dated inflation-linked bonds which should benefit from any pick-up in inflation, and I like credit still because companies have not yet shown any signs of deteriorating fundamentals. As the outlook gets murkier, better-quality credit should be more stable and there will be more expectation that central banks will cut rates further – after all, real rates are still high relative to the experience since the global financial crisis.

Old men

I participated in a webinar with an associate editor of the Financial Times this week. It was fascinating, but gloomy. His opening remark was that, globally, we are half way through the most dangerous decade since the 1940s. One other remark that really stuck was that most of the world’s so-called strong-man leaders – Trump, Vladimir Putin, Xi Jinping, Narendra Modi, Luiz Inácio Lula da Silva, Recep Tayyip Erdoğan, and Benjamin Netanyahu – are all in their 70s. Life expectancy is higher today, of course, and access to the best medical care will help, but at some point there will be a significant rotation of power to a new set of (younger?) leaders. Geopolitical uncertainty is not going away!

(Performance data/data sources: LSEG Workspace DataStream, ICE Data Services, Bloomberg, AXA IM, as of 27 March 2025, unless otherwise stated). Past performance should not be seen as a guide to future returns.

Subscribe to updates

Have our latest insights delivered straight to your inbox

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.