Emerging markets Asia: Picking a side

- 19 September 2024 (5 min read)

KEY POINTS

A friend of the enemy

Emerging markets (EM) Asia will be closely watching the US presidential election. While we see few direct impacts from a Kamala Harris win, a Donald Trump victory would likely pose several challenges for the region.

EM Asia broadly benefited from the 2018-2019 US-China trade war, not only enjoying a more competitive position vis-à-vis Chinese exporters to the US but also attracting foreign investment from firms engaging in “China + 1” strategies and investment from Chinese firms seeking to diversify their supply chains (and circumvent US tariffs).

The region’s favourable position can be attributed to its success in avoiding picking a side. However, if Trump wins, the risk of an escalation in the US-China trade war could see key markets in the region find it difficult to continue to reside in this sweet spot. Trump would be unlikely to tolerate what he may deem an increasingly one-sided relationship with markets that have seen trade surpluses with the US widen and benefited from US regional security backing but simultaneously have built closer economic ties with China. EM Asia could therefore face a tougher trading environment with the US and a reassessment of existing security arrangements if Trump is re-elected.

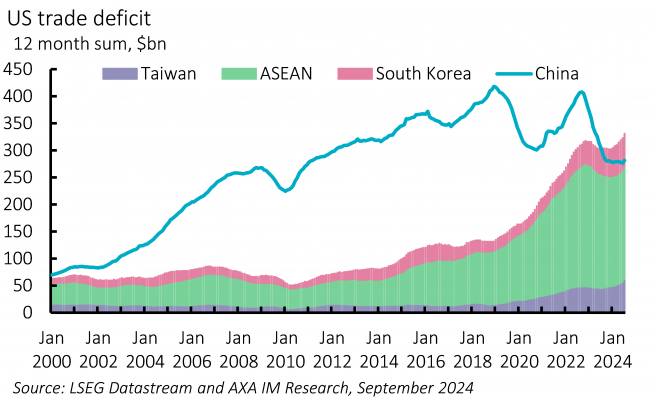

The region now has a much wider trade surplus with the US than in Trump’s first term (Exhibit 6). While some of EM Asia’s gains have come at the expense of China, this also reflects a rewiring of Chinese supply chains to circumvent US protectionist policies, with South-East (SE) Asian nations being notable conduits. This has already played out in solar panels –

a decade or so after the 2012 US tariff hike on Chinese solar panels, SE Asia now accounts for around 80% of all US solar panel imports, much of which is linked to Chinese firms. In August 2023, the US Department of Commerce (DoC) announced the final determination of a circumvention inquiry that found Chinese producers were shipping solar products through these markets for minor processing to avoid paying anti-dumping and countervailing duties.

China’s investment in SE Asia manufacturing facilities has also picked up in recent years. Its total outward direct investment position in Vietnam, Thailand and Malaysia combined rose from US$16bn in 2018 to US$37bn in 2022, according to International Monetary Fund data. More recently, fDi Intelligence reported that in 2023 China pledged US$26.4bn in greenfield projects in the Association of Southeast Asian Nations, up from an annual average of US$7.7bn in 2014-2022. This makes it challenging for the DoC to identify and contain Chinese efforts to circumvent trade tariffs. Tougher anti-China policy could include blanket tariffs on nations deemed to be benefiting from close ties with China (particularly those enabling China’s tariff evasion) – and EM Asia will be a prime target. Complicating further, EM Asia will also need to be wary of cheap Chinese imports; Indonesia has already taken action, imposing tariffs of up to 200% on some Chinese goods.

In addition to hiking tariffs on so-called unfair trade covering China-linked imports, there is a broader risk any future trade negotiations or disputes with a new Trump administration could include threats to withdraw US security commitments, or demand greater contributions towards existing arrangements.

In particular, Korea and Taiwan have also seen trade surpluses with the US widen and these could attract a protectionist response, given Taiwan’s dominant position in semiconductor manufacturing and Korea’s rising vehicle exports to the US. A harbinger of a more complicated relationship with the US was Trump’s comments in July that Taiwan should pay the US for protection from China, while also bemoaning Taiwan’s dominance in global semiconductor trade. Tellingly, in his first term, Trump accused South Korea of free riding on US security support and renegotiated the Korea-US Free Trade Agreement (KORUS) accordingly.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.