Emerging Markets – Tomorrow is another day

- 02 December 2020 (5 min read)

Key points

- Recovery and vaccine. The pandemic’s impact on emerging market (EM) growth dwarfed that of the global financial crisis. Our forecasts see EM ex-China GDP growth down by 5% this year versus +0.7% back in 2008. Recovery in China and advanced economies should grant a better external environment for EMs in 2021 and 2022.

- COVID-19 related fiscal spending averaged 3.8% of GDP in 2020 for EM, support should fade next year

Recovery and vaccine. The rebound is dependent on the evolution of the pandemic, the methods used to tackle the crisis – both locally and globally – and the strength of the policy mix. Growth should rebound +4.5% in 2021 and 4.0% in 2022; output gaps should be closing quicker in the exporting Asian countries, followed by EM Europe, but we expect them to persist well into 2022 in Latin America. We assume an efficient vaccine cannot be widely distributed in EM before 2022, with few exceptions like China, Russia and European Union countries in Central Europe. Still, global mobility is likely to slowly resume from mid-2021 as advanced economies reach herd immunity. Pressure on external financing and currencies should thus ease, allowing EM policymakers flexibility.

Global trade normalisation tailwind. Recovery in China and advanced economies should grant a better external environment for EMs. Export recovery should support manufacturing activity and commodity prices should be under less downward pressure, although we do not expect a demand surge. Services activities, particularly in the sectors directly affected by the pandemic, will take longer to recover. Current account deficits should thus remain contained, in absence of renewed portfolio outflows, limiting stresses on external financing needs.

Slow policy normalisation. COVID-19 related fiscal spending averaged 3.8% of GDP in 2020 for EM, ranging from 0.6% for Mexico to 8% for Brazil. Fiscal support should fade next year but remain expansionary, where fiscal space still allows. EM public debt is expected to reach 65% of GDP by 2021, not overwhelming compared to above-100% debt-to-GDP ratios of several advanced economies, but includes debt trajectories in countries, like Brazil, India or South Africa, where debt trajectories have been propelled towards dangerous spirals, limiting future spending. In a context of persistent output gaps and limited inflation pressures, unconventional monetary policy is also being used to maintain loose financing conditions. Still, quantitative easing (QE) is no panacea. Global recovery may trigger a rise in global interest rates, driving domestic rates higher and rising the financial sustainability risks of highly indebted low-income countries.

Asia ex-China: A two-speed recovery

The pandemic has been a major driver of Asian growth this year. However, the severity of the shock has varied across different countries. The export-dependent economies – Korea, Taiwan, Thailand and Singapore – did a better job at controlling the virus and saw growth rebound quickly from the slump. The domestic-oriented economies such as India, Indonesia and the Philippines are still struggling with the pandemic and face deeper growth contractions.

The outlook for these two groups of economies should also vary in 2021. The export-dependent group is expected to see a faster normalisation of domestic activities – thanks to better coronavirus management and possibly a vaccine – along with strong tailwinds from recovering external demand. In contrast, the domestic-oriented group is expected to endure a lingering pandemic that holds back their growth recovery. Altogether, we expect economic growth in Asia (excluding China) to rebound to 5.8% in 2021, after a 4.9% contraction this year, before normalising to 4.3% in 2022.

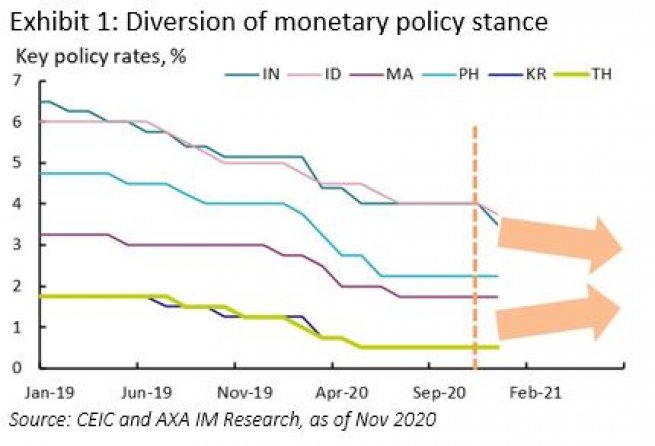

Inflation has dropped to multi-year lows following the shock this year. Central banks reacted by aggressively slashing interest rates and implementing large liquidity/credit injections. While a growth recovery will support inflation in general, we expect a divergent monetary policy stance between the two groups of economies (Exhibit 1). On the back of a faster recovery, central banks in Korea, Taiwan and Thailand should start to exit policy accommodation in the second half of 2021. In contrast, more easing – with rate cuts to the tune of 25 to 75 basis points (bps) – is expected in India, Indonesia, the Philippines and Malaysia, where growth headwinds warrant further monetary support. Fiscal policy will remain expansionary, after having been extensively used this year. As fiscal room shrinks across the region, some countries will be positioned for consolidation in 2021.

Exhibit 1: Diversion of monetary policy stance

Latin America: The faster you go nowhere, the less time you take to get somewhere

The post-pandemic recovery in Latin America will be as varied as countries’ reactions to the virus, but the return to sustainable growth in the region remains a common trait.

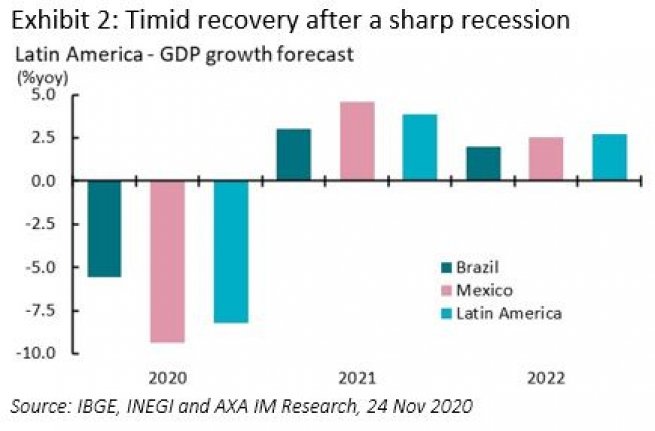

The fragile economic and social situations of the South American countries caused a greater shock than elsewhere. The diversity of government responses outlines different recovery paths for each economy. Although the average government pandemic response in the zone was 3.4% of GDP, the dispersion was wide, with Brazil (8.3% of GDP) the country with the strongest fiscal support while Mexico the lowest spender (0.6% of GDP). Although the average government pandemic response in the zone was 3.8% of GDP, the dispersion was wide, with Brazil (8.3% of GDP) the country with the strongest fiscal support while Mexico the lowest spender (0.6% of GDP). In 2020, this materialised into a stronger contraction for the latter (-9.4%yoy) than Brazil

(-5.4%) and the whole area (-8.2%). However, the reaction of central banks nuances these differences. Indeed, after having sharply lowered their key rates, monetary conditions should remain accommodating into the first half of 2021.

Exhibit 2: Timid recovery after a sharp recession

Major local political and economic challenges have emerged for the coming years. In Brazil, despite the strong activity recovery expected, the extraordinary government spending creates an important fiscal challenge. The potential creation of the 'Renda Cidadã' programme adds pressure to government spending plans for 2021, casting doubt on the ability to follow the spending cap, exceptionally repealed for 2020 and jeopardizing the future fiscal development of Brazil. We forecast growth of 3.9% for Brazil in 2021. In Mexico, the stakes are diametrically opposed. The government's fiscal prudence has kept public finances strong but has penalised the recovery in domestic activity. With a supportive central bank and the recovery of the US, Mexico’s main trading partner, we forecast a 4.6% annual rebound in 2021 (Exhibit 2).

The busy political calendar – legislative elections in Mexico (2021), a referendum and general elections in Chile (2021) and presidential elections in Brazil (2022), adds uncertainty to the already fragile future in Latin America.

Emerging Europe: Recovery post second wave

Central and Eastern Europe (CEE) swiftly managed the spring coronavirus wave by implementing lockdowns at very early stages. The re-opening of the economies drove a strong recovery in Q3 2020. The recent revival of the virus across Europe, which called for renewed lockdowns, will impact growth negatively in Q4 2020 to Q1 2021, postponing the recovery. The region, as part of the European Union (EU), could benefit from fiscal support via the European Recovery Plan in addition to the EU budget directed towards them if/when the current blockage gets resolved – and from available healthcare responses, including treatments and any vaccines, which should all further support economic activity. Monetary policy is likely to lean on the dovish side for longer as inflation pressures are expected to recede. We then see slow policy normalisation starting towards end-2021 or even 2022. Growth is expected to rebound 4.1% in 2021, after -4.1% in 2020.

The COVID-19 induced recession was relatively shallow in Russia. Looking ahead, as global growth recovers, there should be less pressure on commodity prices, but we do not envisage a particularly strong recovery in oil production. Short term inflationary pressure stemming from currency pass-through should recede, and the central bank may even cut rates by an additional 25bp next year. Domestic demand remains fragile and a resurgence in infection throughout Europe, including Russia, makes us less optimistic about a strong rebound next year (+1.5% expected). On a positive note, Russia appears likely to be able to distribute an anti-COVID-19 vaccine at an earlier stage than most EM peers.

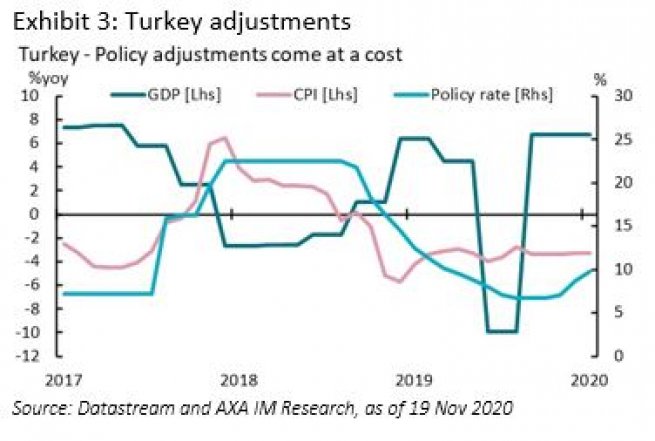

Turkey’s expected 2% GDP contraction this year looks particularly good when compared to most countries. Yet inflation slippage caused by an overstimulation of activity pre-dating and exacerbated by the pandemic are being addressed. The central bank’s foreign exchange reserves are running low and external financing needs are running high. Recently, the central bank hiked interest rates by 475bps and simplified its framework. We expect further tightening to take its toll on economic growth at the start of 2021, and forecast +3.5% GDP growth, normalizing to +4.6% in 2022 (Exhibit 3).

Exhibit 3: Turkey adjustments

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.