What is the future of a cashless society in a post-COVID-19 world?

Advancements in technology have revolutionised how consumers and financial providers interact with one another. The emergence of fintech firms, which have created real-time, seamless solutions, mean that payments are now possible without banks or handing over cash.

Combined with continued growth in e-commerce, this has led to an upward trajectory in the volume of contactless transactions, notably over the past decade. And since the start of this year, the coronavirus pandemic has prompted a surge in cashless payments as consumers are driven online as a result of lockdowns, or try to avoid handling cash for fear of transmitting the disease.

This has changed the way businesses are operating with consumers, with payments companies playing a key role in this transition.

Lockdowns have accelerated online sales

As the coronavirus outbreak has become more widespread, sending huge swathes of the global population into lockdown, more people are shopping online for anything from necessities such as food and medication, to entertainment.

Global retail e-commerce sales experienced 209% growth in April 2020, compared to the same period in 2019, according to research from ACI Worldwide.1 Amazon posted revenues of $75.4bn in the first three months of 2020, equivalent to over $33mn per hour.2 Moreover, US consumer spending on online electronics has shown no signs of deceleration, up 111% to over 142% year-on-year to 29 May 2020.3 Elsewhere, China’s online grocery market is now expected to grow 62.9% in 2020, compared to a 29.2% growth in 20194, led by the likes of Alibaba and Tencent-backed JD.com.

In the wake of the pandemic, even smaller retail businesses have started to develop models to facilitate clients ordering online, for example through social media platforms. Facebook recently launched Shops, which will allow businesses to display and sell their products on the platform5 – beneficial for firms who have been forced to close bricks-and-mortar stores due to the virus. In China, businesses have taken to livestreaming video in order to sell directly to consumers, with the number of e-commerce livestreaming sessions reaching four million in the first quarter.6

Naturally, increased online shopping leads to a surge in demand for digital payments providers. For example, for PayPal, 1 May marked the largest single day of transactions in the company’s history – bigger than both Black Friday and Cyber Monday of 2019. The firm added 10 million net new active accounts to its core platform in the first quarter of 2020, with 7.4 million in April alone, a new monthly record. For the second quarter, it projects a further 15-20 million net new active accounts.7

Meanwhile, Visa recorded 13 million cardholders in Latin America make e-commerce transactions for the first time in the first quarter – representing around two in 10 active cardholders in the region. Visa also saw an 18% rise in US digital commerce spending (excluding travel) in April.8

The death of cash?

It’s not just online platforms where digital payments are the obvious method of transaction. Even on the high street, consumers are increasingly paying with cards, not cash – in part, to try to reduce the transmission of coronavirus. The European Union’s banking watchdog has encouraged payment firms to increase contactless payment limits from €30 to €50 per transaction for this very reason.9

Moreover, in March, the World Health Organization recommended that people turn to cashless transactions to fight the spread of COVID-19.10

The concept of a cashless society, however, isn’t new. Sweden is arguably the most advanced cashless society in the world, with around 1% of its GDP circulating as cash.11 Meanwhile, 2019 was the first year in which more than half of payments in the UK were made by card.12 Elsewhere, the influence of innovative apps such as Alipay and WeChat Pay on consumers in China has been significant, with 81% of smartphone users using proximity mobile payment services.13

The number of worldwide non-cash transactions annually is forecast to pass one trillion in 202214 and amount to $5.7 trillion15, around a three- and five-fold increase from 2013, respectively.

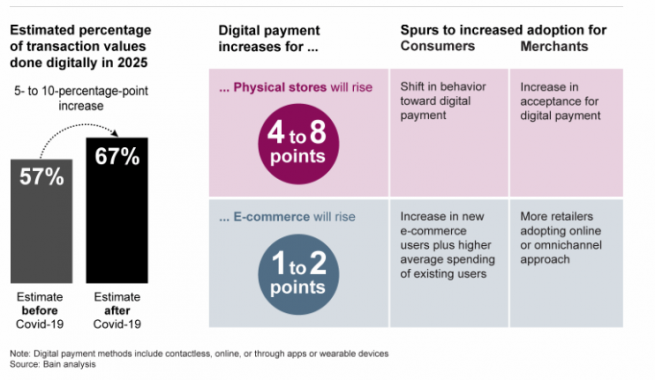

A recent report from Bain & Company estimates that the adoption of digital payments could see a five- to 10-percentage-point increase globally, by 2025. While COVID-19 may have spurred faster growth of this trend, it is a structural change.

- Global eCommerce Retail Sales Up 209 Percent in April, ACI Worldwide, 12 May 2020

- Amazon posts $75bn first-quarter revenues but expects to spend $4bn in Covid-19 costs, The Guardian, 30 April 2020

- BAC credit card data shows no deceleration in online electronics spending/limited deceleration in online retail spending where economy re-opened, BofA Securities, 4 June 2020

- E-commerce drives China's stay-at-home economy in coronavirus aftermath, S&P Global Market Intelligence (stats from iiMedia Research), 23 March 2020

- Facebook Shops: Online stores open on Facebook and Instagram, BBC News, 19 May 2020

- Livestreaming is taking off in China, but it’s not driving much sales in a market still reeling from coronavirus, CNBC, 29 April 2020

- PayPal says May 1 was largest transaction day in its history, but first-quarter results fall short, MarketWatch, 7 May 2020

- Visa sees massive digital acceleration with millions trying e-commerce for the first time, MarketWatch, 18 May 2020

- Contactless payments can help cut contagion – EU banking watchdog, Reuters, 25 March 2020

- WHO encourages use of contactless payments due to COVID-19, Forbes, 9 March 2020

- Payments in Sweden in 2019, Riksbank, 7 November 2019

- More than half of all payments made by card even before coronavirus, BBC News, 3 June 2020

- China mobile payment users 2019: Moving toward a cashless society, eMarketer, 24 October 2019

- World Payments Report 2019, Capgemini

- Retail e-commerce sales worldwide from 2014 to 2023 (in billion US dollars), Statista 2020

Trust is key for consumers

The ability to shop online has become of paramount importance for many consumers living under lockdown while for others, it was already a way of life for reasons ranging from convenience to choice. Digital adoption has grown as a result of these government measures, even among those who aren’t digital natives.

However, while the COVID-19 crisis has shone a light on the e-commerce industry, it has also potentially opened a door to greater levels of online fraud. It is, therefore, imperative that payment companies, and every business that accepts payments online, take necessary fraud prevention measures to protect their customers. And while trust in terms of data privacy is hard won, it can be easily lost.

A continually evolving retail landscape

The shift from physical retail to online, which was already firmly underway, will undoubtedly accelerate as a result of the crisis. With businesses around the world now embedding digital solutions within their infrastructure to cater to their customers’ needs, we expect this is a revolution that will not diminish, and will continue to drive a strong increase in digital payments. Furthermore, we expect that once consumers have tried contactless payments and see how simple, safe and efficient it is, they are very unlikely to revert to cash payments.

We expect a temporary decrease in offline digital payments due to lower payment volumes in a number of impacted areas such as travel and hospitality, but believe there will be moderate growth in overall digital payment volumes in 2020 – and they could even accelerate quickly thereafter. We see digital payments firms with a global footprint as the main beneficiaries, with the crisis favouring highly cash-generative businesses that can demonstrate resilience in such circumstances. We also expect such firms to gain a larger market share over the coming years as smaller players disappear or are acquired, creating more concentrated and profitable markets for the winners.

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This promotional communication does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee that forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Before making an investment, investors should read the relevant Prospectus and the Key Investor Information Document / scheme documents, which provide full product details including investment charges and risks. The information contained herein is not a substitute for those documents or for professional external advice.

The products or strategies discussed in this document may not be registered nor available in your jurisdiction. Please check the countries of registration with the asset manager, or on the web site https://www.axa-im.com/en/registration-map, where a fund registration map is available. In particular units of the funds may not be offered, sold or delivered to U.S. Persons within the meaning of Regulation S of the U.S. Securities Act of 1933. The tax treatment relating to the holding, acquisition or disposal of shares or units in the fund depends on each investor’s tax status or treatment and may be subject to change. Any potential investor is strongly encouraged to seek advice from its own tax advisors.

Past performance is not a guide to current or future performance, and any performance or return data displayed does not take into account commissions and costs incurred when issuing or redeeming units. The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested. Exchange-rate fluctuations may also affect the value of their investment. Due to this and the initial charge that is usually made, an investment is not usually suitable as a short term holding.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.