The critical role of ETFs in providing liquidity and facilitating price discovery amid market stress

- 28 April 2025 (5 min read)

KEY POINTS

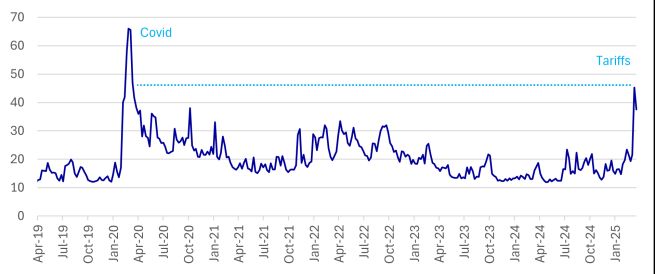

US President Donald Trump announced a wave of new tariffs on 2 April, which he branded ‘Liberation Day’, arguing they would help boost the US economy. At this stage, uncertainty around trade policy, global growth, and inflation remains very high. It is impossible to predict exactly when markets will start to stabilise, and this has triggered a huge increase in volatility across financial markets globally. This uncertainty is highlighted by the Cboe Volatility Index (VIX), which recently closed at its highest level since April 2020, during the early months of the Covid-19 pandemic. The MSCI ACWI index dropped by 11% between 2 April and 8 April 2025. For many indices, it was the worst week since the Covid days, while over $5Trn in market value was wiped off the S&P 500 in the last two sessions of the week1 .

- U291cmNlOiBCbG9vbWJlcmcgYXMgYXQgOCBBcHJpbCAyMDI1ICA=

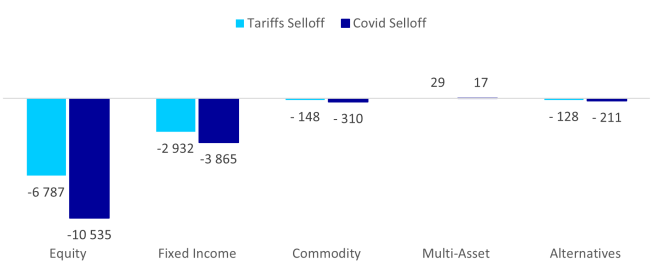

Relative resilience of ETF flows following tariffs announcement versus Covid selloff

Despite markets experiencing the type of performance and volatility unseen since the Covid-19 pandemic, ETF flows in recent weeks indicate that investor reactions have been more measured following the announcement of tariffs.

Equity ETFs bore the brunt of the outflows during both periods, but an additional $4bn outflows was recorded during the initial Covid selloff. Overall, withdrawals across all asset classes have been significantly lower than those seen five years ago.

Investors are looking for safe heavens

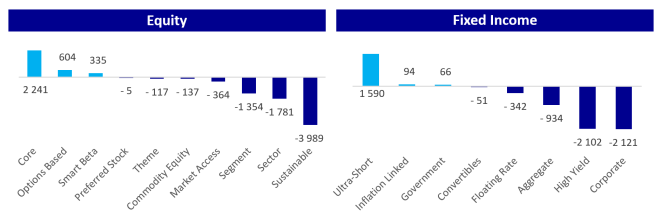

Core ETFs saw net positive flows of $2.2bn (2to 11 April)2 . Investors traded their US exposure in preference for Europe and Japan, areas that may present a better economic outlook. They also swapped out riskier ETFs as the markets declined. Sector and sustainable ETFs landed in negative territory. Option based UCITS ETFs, especially on US equities, gathered positive flows of $604mn in this period. Emphasising the ‘buy-the-dip’ mentality and an anticipated rebound in tech stocks from investors.

The shift toward safety was more evident in fixed income. Investors favoured low credit-risk segments such as ultrashort maturity (+$1.5bn) and government bond ETFs (primarily US TIPS) while looking to avoid the stock market decline. On the other end of the spectrum, high yield (-$2.1bn) and credit ETFs lagged, as these assets are generally more correlated to the stock market.2

- U291cmNlOiBFVEZCb29rIGFzIGF0IDExIEFwcmlsIDIwMjU=

- U291cmNlOiBFVEZCb29rIGFzIGF0IDExIEFwcmlsIDIwMjU=

Active ETFs weather the shock

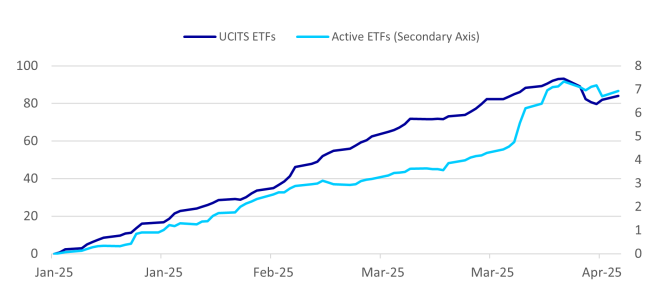

Following the announcement of tariffs on 2 April, UCITS ETFs saw outflows, with over $11bn withdrawn in just one week from the $92bn already collected year-to-date. In the same period in 2024, UCITS ETFs had gathered $56bn year-to-date, and $46bn in 2023. 2025 is already a record-breaking year for the UCITS ETF industry with flows as of 11 April being at $89bn despite the tariffs selloff, which had a relatively small impact.2

During the same period from 2 April to 9 April 2025, however, actively managed ETFs experienced a positive inflow, with a net inflow of $20mn adding to the $7Bn collected year-to-date. This indicates that investors moved away from passive ETFs while actively managed ETFs displayed stability.2

- RVRGQm9vayBhcyBhdCAxMSBBcHJpbCAyMDI1

- RVRGQm9vayBhcyBhdCAxMSBBcHJpbCAyMDI1

ETF liquidity as an answer to market volatility

Such heightened volatility creates a challenging environment for investors, prompting them to seek effective solutions for navigating these turbulent times. In this context, the importance of ETFs becomes evident. According to ETFBook, in the week following 2 April, UCITS ETF trading volume surged to $191bn - a striking two-fold increase from $101bn the week prior to the announcement. The peak was reached on the Monday 7 April as markets reacted to additional tariff announcements following the closing of the market in China at the end of the previous week, with $45bn in volume compared to an average $19bn in daily volume in March.2 This dramatic rise emphasises the critical role of ETFs in providing liquidity and facilitating price discovery amid market stress.

In just two weeks of April, AXA IM’s ETF range recorded its third busiest month on record, with orders volume totalling $173mn following Donald Trump’s 'liberation day’. This activity highlights how AXA IM’s UCITS ETF product range and capabilities can effectively meet investors' liquidity needs during periods of volatility.3

Despite recent outflows in the UCITS ETF market driven by concerns over equities and fears of a global recession, the substantial uptick in trading volume illustrates that investors continue to turn to ETFs to meet their trading needs during these volatile periods.

- U291cmNlOiBFVEZCb29rIGFzIGF0IDExIEFwcmlsIDIwMjU=

- U291cmNlOiBFVEZCb29rIGFzIGF0IDE0IEFwcmlsIDIwMjU=

Subscribe to updates

Have our latest insights delivered straight to your inbox

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© 2025 AXA Investment Managers. All rights reserved

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.